Greenwich Real Estate 2024 Year in Review and 2025

Mark Pruner | January 7, 2025

Market Report

Mark Pruner | January 7, 2025

Market Report

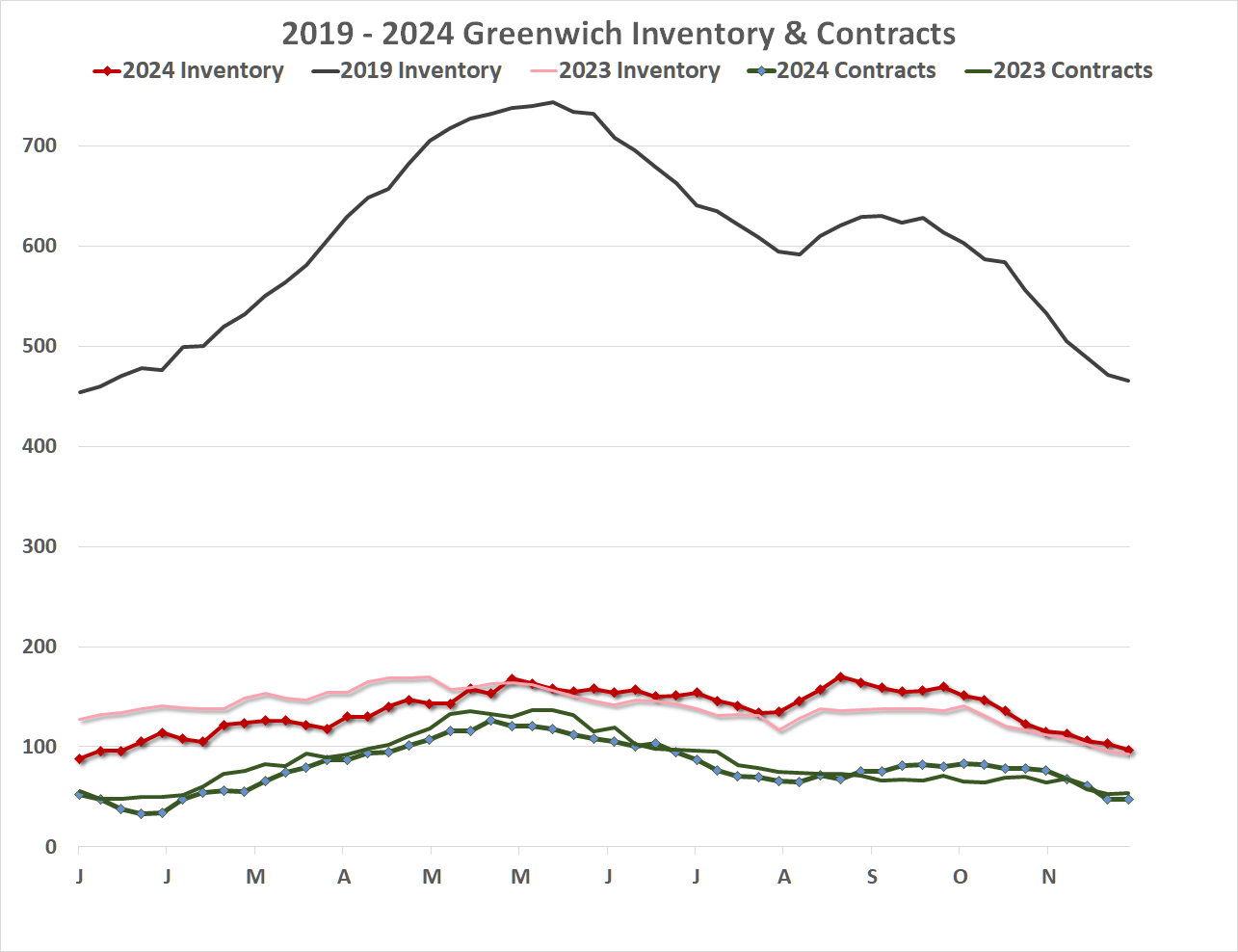

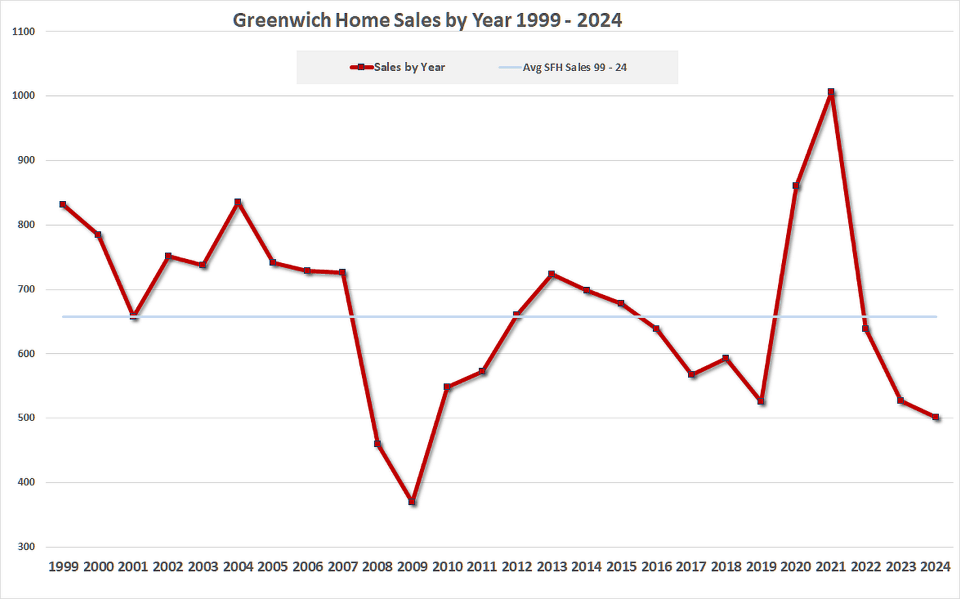

At the beginning of 2025, two things happened to the Greenwich real estate market that had never happened before. First, our inventory of single-family homes fell to only 86 listings, a new all-time low. For comparison, if you go back to our last pre-Covid year, we opened 2019 with 454 listings. We are down 81% from 2019 or to put it another way, we had over five listings for sale in January 2019 for every one listing that we have today.

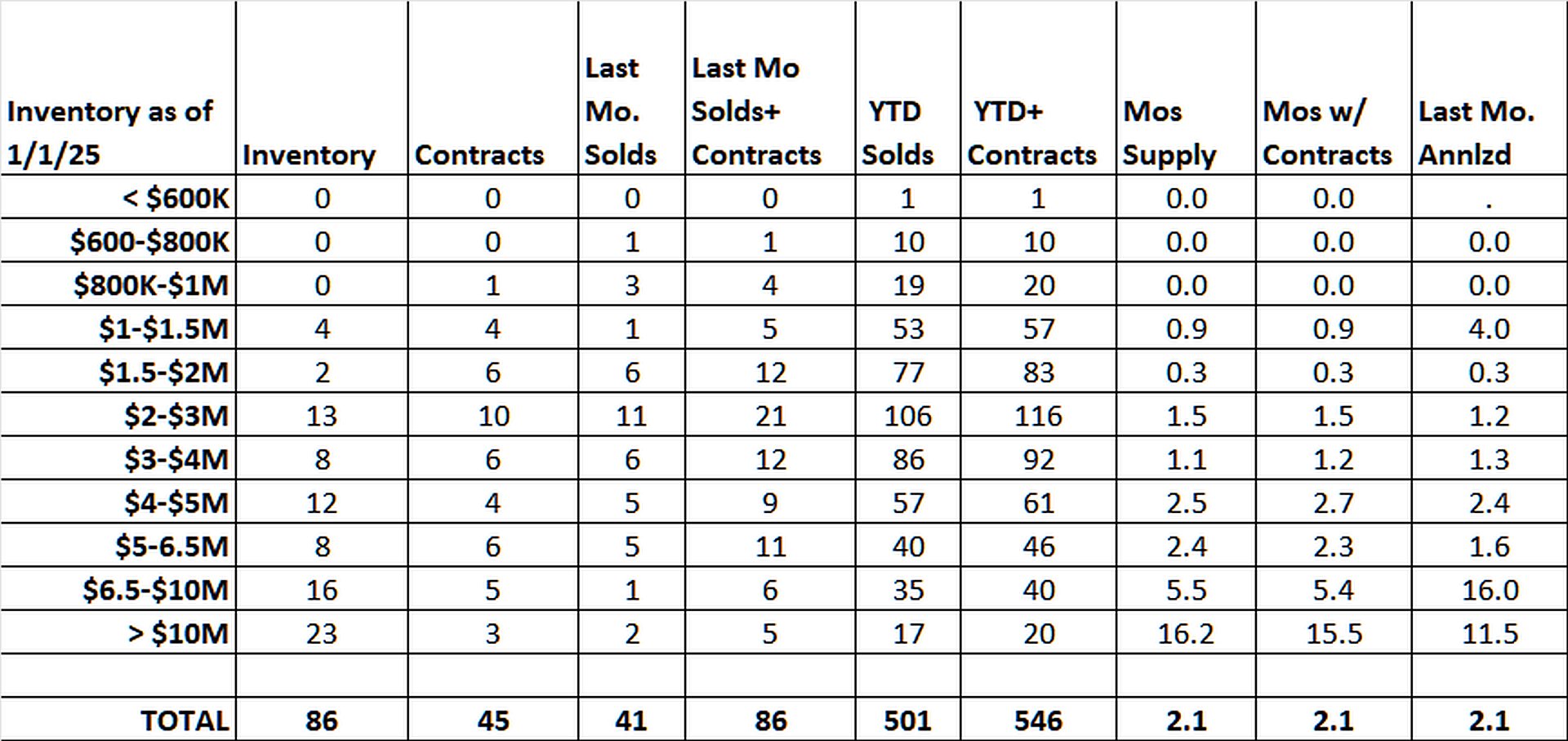

The other thing that had never happened was that we had no single-family home listings priced under $1 million. Out of the 86 listings we have at the beginning of the 2025, the lowest priced house listing was $1,099,000 for a 2,500 s.f. house in Pemberwick. In 2021, it expired unsold for $885,000. The next lowest priced house is on for $1,295,000 in Glenville. We then have 2 houses priced at $1,350,000. Which means, under $1.35 million you have four choices and 3 of those 4 houses have been on for less than a month. (You do have a choice of 13 condos and co-ops, 12 of which are in central Greenwich and all of which are at least 50 years old.)

While we presently have no listings under $1 million, we did have 30 house sales last year for under $1 million. This is down from 59 sales in 2023 under that price. Of our 30 sales under $1 million, the median days on market was 36 days. As this is by far our hottest market, I thought they would get to contract even quicker given that our median days on market for all sales is an amazingly low 22 day. This anomaly bore some further checking.

It turns out that our sales under $1 million did get to contract faster. When you look at those 30 sales, 16 of them, or just over half, had a contingency, generally a mortgage contingency. For those properties, our MLS software provider treats these listings as still on the market, even though they are under contract. They continue to accumulate days on market until the mortgage contingency is removed. When you exclude the sales under $1 million without a mortgage contingency, those 14 listings got to a binding, non-contingent contract in 16 days, even faster than the median 22 days on market for all house sales.

The other thing that this means is that for those houses priced under $1 million with a mortgage contingency the contingencies were being removed in an amazingly quick 14 days on average. The mortgage companies that are winning business in this hot market are moving much faster to get mortgages approved. (Last year in a multiple offer situation, my client and I got a mortgage commitment in 7 days from her initial meeting with the bank.)

The other thing it means is that lots of buyers are coming in already underwritten pre-approved for a mortgage. In that case all the bank needs is the mortgage appraisal to finish the mortgage approval process. If you need a mortgage to buy a house in this market, you want to get fully pre-approved. It’s the best way to compete with all-cash offers from other buyers.

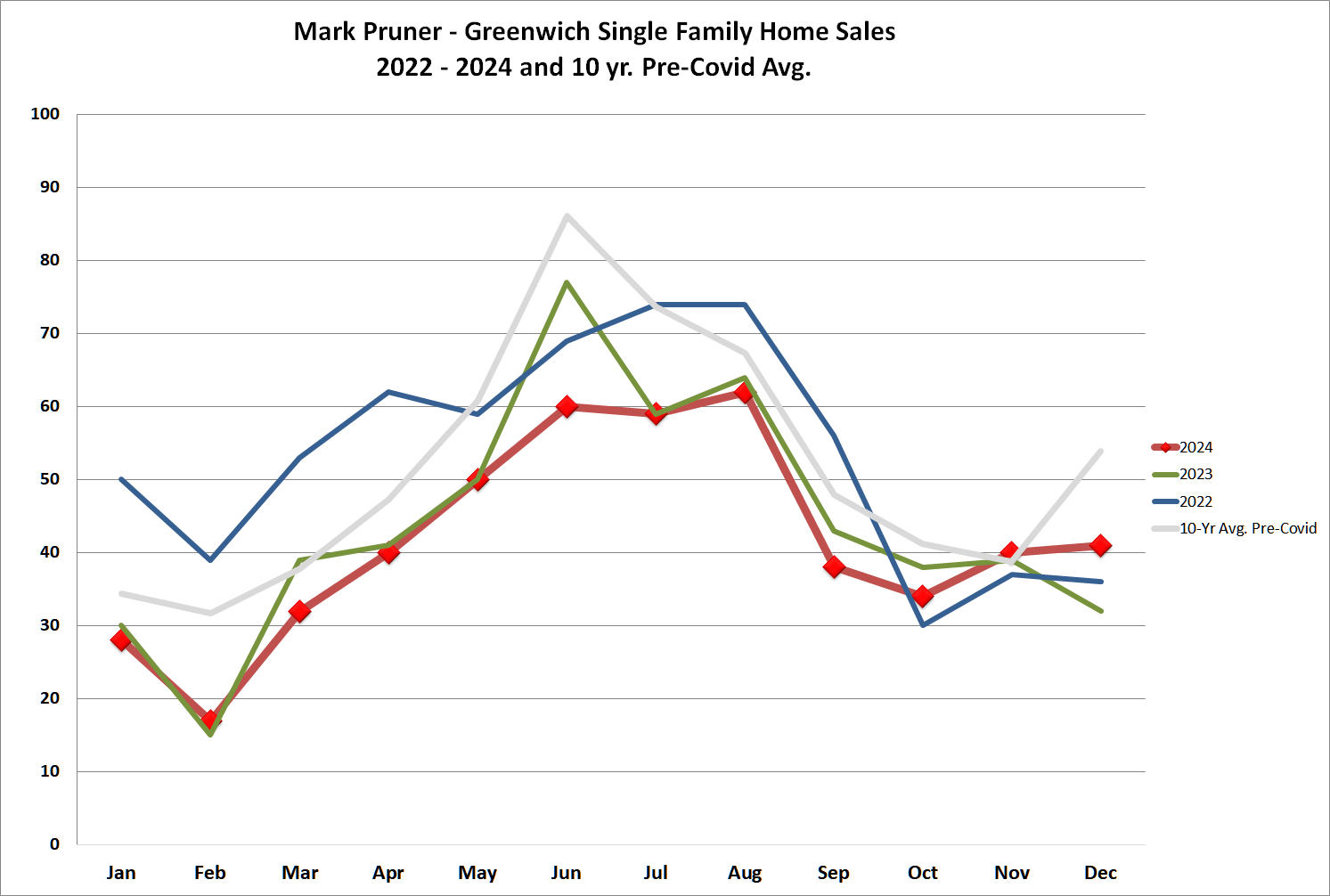

To further show how hot 2024 market was, take a look at our days on market over the last several years. In 2019, the median house stayed on the market for 5 months or 149 days. Two years ago in 2023, our median days on market was down to 5 weeks or 37 days to be precise. Last year in 2024, our median days on market had dropped an additional 40% to only 3 weeks on market or 22 days to be precise.

Some of the finance types out there are going to ask how could the under $1 million market have a median days on market of 37 days as reported above, while the overall market has only 22 days on market. Don’t high end houses stay on market longer?

If you remember from above, our GMLS software provider continues to count days on market even though the house is under contract, if the contract has a contingency. The explanation of fewer days on market above $1 million is that we have more all-cash deals. Only 36% of our deals over $1 million had a contingent contract compared to 53% under $1 million. Also, many of these “contingencies” for higher end houses are not mortgage contingencies, but other issues that often can be checked out in couple days. (I once had a one-week llama contingency to see if llamas could be kept on the property. (The could.))

Last year, like 2023, homeowners were just not listing houses. In Greenwich, only a small part of this is due to homeowners with low interest rates, who are reluctant to move. Yes, interest rates went up, and yes, some people didn’t want to trade in their 3.5% mortgage for a 6.5 % mortgage and its higher monthly payments. But most of the Greenwich buyers didn’t have that problem, since many of them are downsizers, first time homebuyers, beneficiaries or just doing really well.

Lots of Greenwich buyers are downsizers from Westchester County, fleeing the highest property taxes in the nation to buy in Greenwich with some of the lowest property taxes in the tri-state area. Lots of these downsizers paid off their mortgages years ago and are sitting on huge amounts of equity. These downsizers are part of the 62.5% of purchasers in Greenwich that are paying all cash.

The first-time homebuyers are only concerned about whether they can make the monthly payments and have enough cash for the down payment. In Greenwich, many of these first-time home buyers have invested really well, have stock options, a large inheritance or have parents that are the generous type. They don’t have a house to list, and hence aren’t locked in by low-rate mortgages.

Many of our homeowners do have low-rate mortgages, but they also have done pretty well over the last few years in the stock, futures, options, and crypto markets. Some of these folks are taking money off the table and putting it in Greenwich real estate, and some realize that you a bigger house is needed more than a bigger, but risky investment portfolio. For these folks, losing a low-rate mortgage is more than offset, but what they are gaining.

This low inventory led to lower sales in the first three quarters of 2024. For the first half of the year our inventory was below what we saw in 2023. In the third quarter we saw a slight rise in inventory compared to Q3 2023. This resulted in a slight increase in sales in Q4 2024. Overall, we had 501 house sales in Greenwich is 2024, this is down 5% from 2023.

A promising sign is that sales were up 5.5% in the fourth quarter last year. However, these increased sales came from several contracts that closed in December, leaving us with 45 contracts compared to 53 contracts at the end of 2023. Basically, Q4 is a wash.

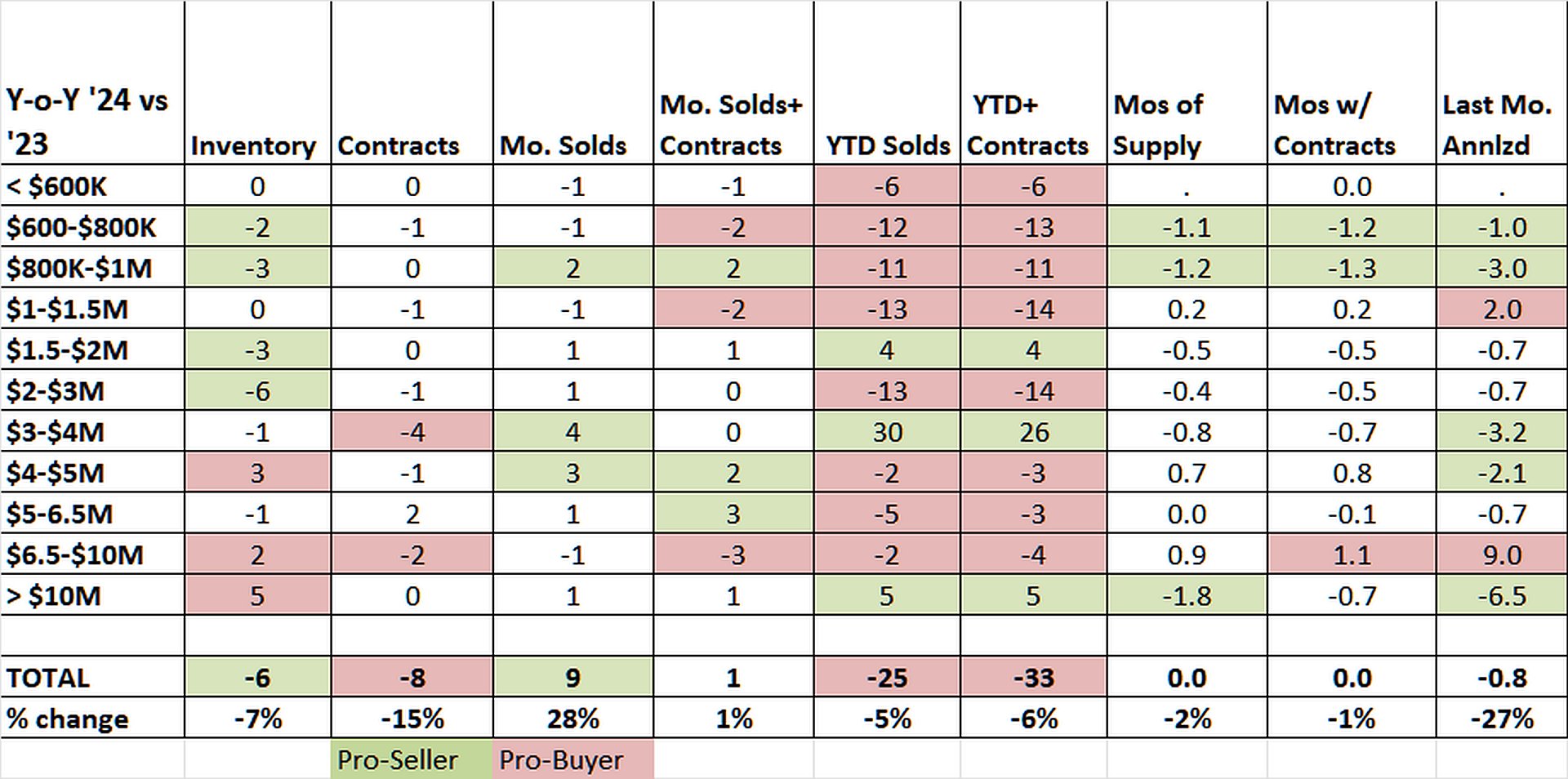

The best market in Greenwich last year was the $3 – 4 million market, which was up 54% in sales. (It was followed by the over $10 million which was up 42% last year, but more about that later.) Our $3 – 4 million market was up, because we had more inventory and hence more to sell. In 2023, we had 56 sales from $3 – 4 million, while last year sales jumped by 54% to 86 houses solds in that price range.

Our sales, from $2 – 3 million, are the heart of our market and unit sales were down 11% from 119 sales to 106 sales. Part of the explanation for that 11% drop in sales is due to 54% rise in sales from $3 – 4 million. Appreciation pushed inventory from the $2 -3 million price range to $3 – 4 million price range. The result was more $3 – 4 million sales and slightly fewer $2 – 3 million sales.

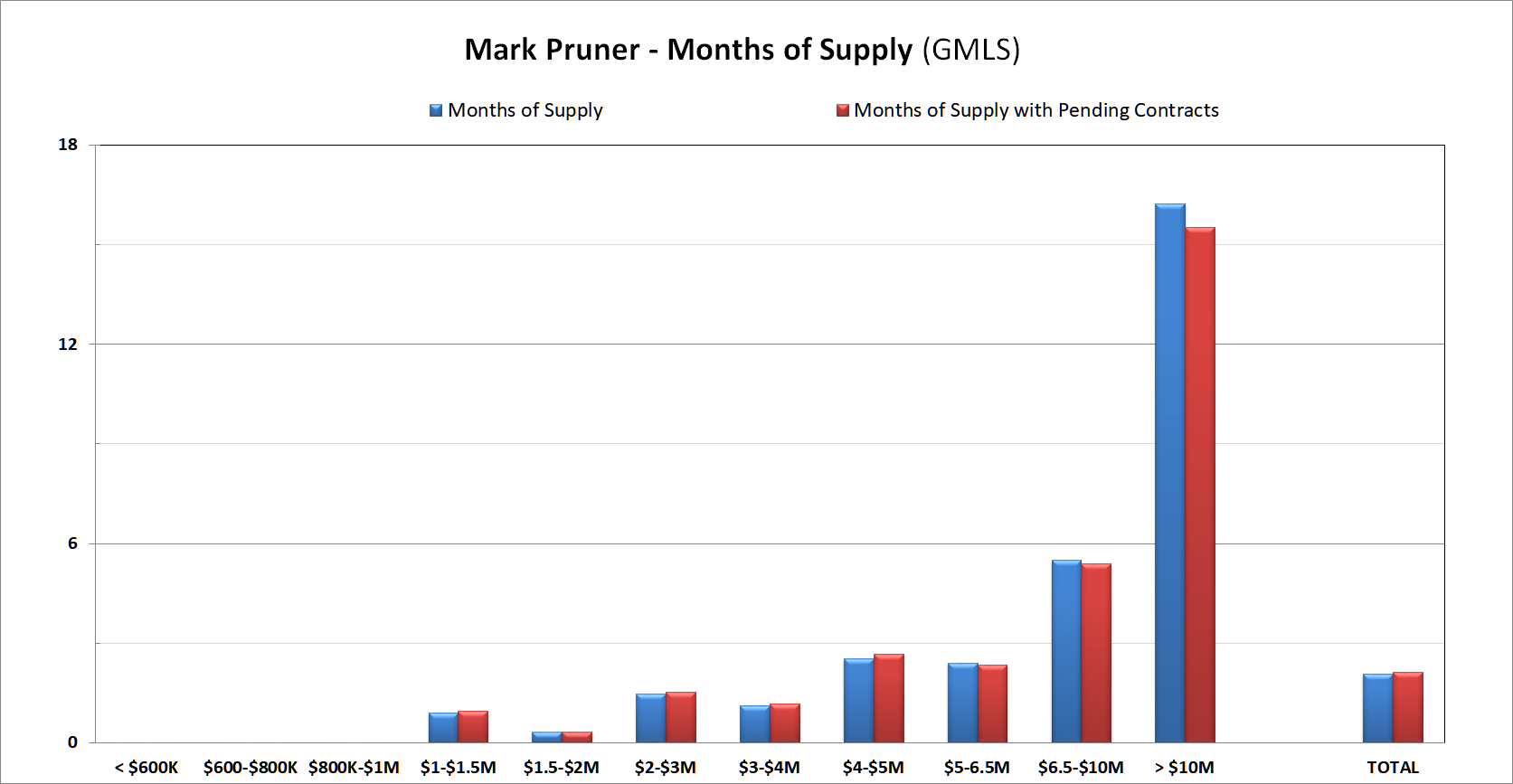

Our market from $5 – 6.5 million is a hot market with only 2.4 months of supply. From $6.5 to $10 million our market slows a bit with 5.5 months of supply. Looking from $5 – 10 million sales are down from 82 sales in 2023 to 75 sales in 2024. This 9% drop is counterbalanced by the aforementioned 42% increase over $10 million from 12 to 17 sales. Totaling everything up, sales prices over $5 million moved higher, while sales were about the same, but we are definitely seeing more interest at the ultra-high-end.

Since we have more than enough buyers for the limited number listing that we have, prices are up again this year. The price appreciation in 2024 is 14.7%, 10.1% or 8.1% depending on which metric you prefer. The median sales price showed this biggest price jump. It went up 14.7% from $2.50 million in 2023 to $2.87 in 2024. Much of this jump in median sales price was a change in the mix of what was selling. In 2024 we had more inventory and hence more sales over the 2023 median. We also had fewer under the 2023 median of $2.5 million. A lot of that was due to the h 50% drop in sales under $1 million.

More high-end sales and fewer sales below median will pull the median up, even if the value of individual houses has not gone up. Two other numbers that are less affected by the shift in the market are the sold price/sf and the sales price to assessment ratio. Our sales price/sf went up from $705 in 2023 to $762/sf last year or an increase of 8.1%. The other ratio takes the sales price and divides it by the Tax Assessor’s assessment for each property. When you compare the 2023 ratio to the 2024 ratio, you come up with an increase of 10.1%.

Increasing equity is key for homebuyers. Back when I was growing up in Greenwich, houses appreciated consistently each year building equity. People bought new houses every 5 to 7 years with this increased equity.

We are seeing some of that come back, as once again, Greenwich houses are seeing significant appreciation year after year. This has led to more Greenwich homeowners looking for houses to buy with all of this equity. For example, if your house has gone up from $1 million to $1.5 million you have $500,000 of equity, that is a 20% downpayment on a $2.5 million house (not counting transaction costs).

For too many people, this equity is locked up, as they have nothing to buy. The resulting low inventory leads to low inventory as buyers won’t list until they know where they are going.

What will 2025 bring? What I can be sure of is we will continue to have well below-average inventory. Inventory will go up as the spring market kicks in, but whether it peaks at 170 listings, as it did this year, or doubles that to 340 listings, it is still going to be well below our pre-Covid inventory levels.

Barring a recession that kills demand, prices will continue to rise as demand continues to exceed supply. Interest rate direction is another matter. It looks like Washington will continue to run major deficits, it is just a question as to whether they will be huge deficits or just really large deficits. The government is going to have rollover more and more bonds and the world is likely to require higher interest rates to keep buying them.

The big question for Greenwich sales however is not interest rates, but how well our financial markets do. If the financial markets continue to do well, then the Greenwich real estate market will very likely to do well.

Mark Pruner is a founding member of the Greenwich Streets Team at Compass. He can be reached at 203-817-2871 or [email protected] or at the Compass office at 200 Greenwich Ave., Greenwich, CT 06831

Stay up to date on the latest real estate trends.

Blog

What RealTrends Verified Actually Means for the Greenwich Streets Team

Blog

Blog

Blog

What the Numbers Actually Mean for You

Blog

What Every Greenwich and Stamford Pet Owner Should Know

Blog

What Actually Matters (And What Doesn't)

Market Report

Stamford, CT

We have 8 options for you

Blog

Discover the best places to live across Greenwich

We are a dedicated group of Greenwich natives. We have a deep passion for our hometown and enjoy everything the town offers its residents from the beach front to the backcountry. That is why we don’t find you just any home, we find you the right home.

MARK PRUNER

DENA ZARRA

RUSSELL PRUNER

COMPASS

200 Greenwich Ave

3rd Fl Greenwich, CT 06830