Inventory Down, Sales Up

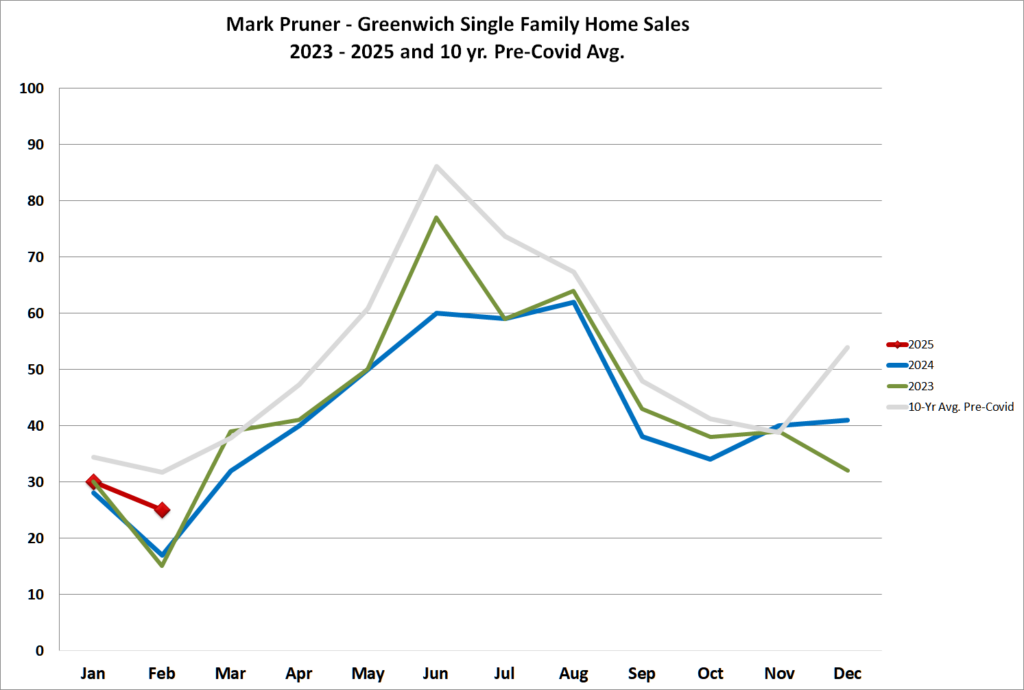

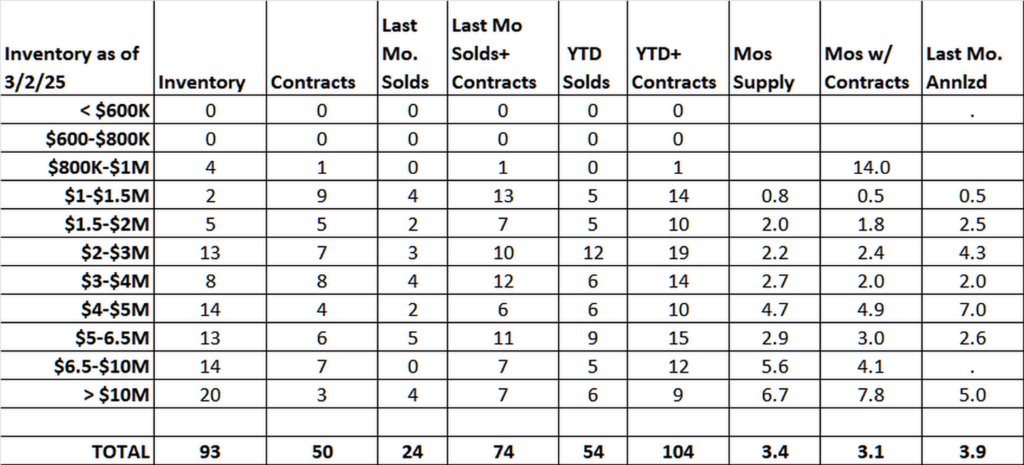

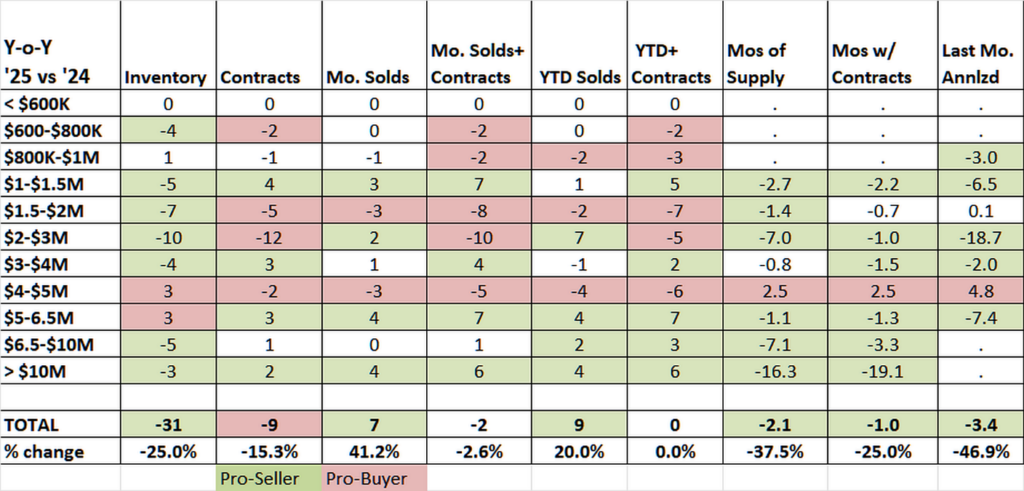

February 2025 was a remarkable month. We sold 47% more houses than in February 2024, despite having 25% less inventory than last year. By the numbers, we sold 25 houses last month compared to 17 houses in February 2024. At the same time, we ended February with only 93 single-family homes on the market, down 25% from 2024. At the end of February 2024, we had 124 single-family homes on the Greenwich MLS, which was an all-time record low for the end of February.

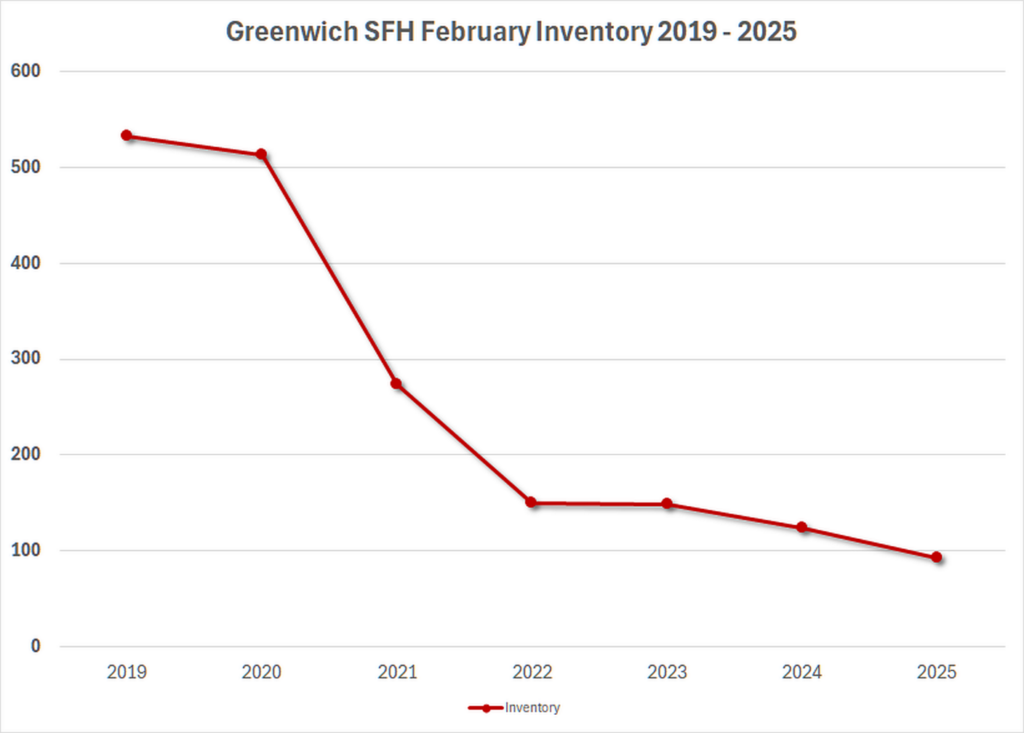

Come the end of February 2025, we set a new all-time record low for the end of February, and not just by a little bit. We had a drop of 31 houses or a 25% decrease year over year. The inventory was actually not even that good, as out of 93 listings at the end of February, 65 of them, or 70%, had been on the market for more than a month. In a market this hot, if you don’t have a contract or at least significant offers within the first 30 days, you are probably overpriced or there is some other problem.

It could be that you have an old house that needs work, a house style that is not popular, a strange lot shape or wetlands that make it difficult to determine what a buyer could build on the property without filing with the Zoning Board of Appeals or Inland Wetlands. All of those issues, and more, can be cured by simply reducing the price. Alternatively, you can do the work, change the style of the house, or get the permits yourself, but most of the time, lowering the price is the better option, since the issue that you as the seller solve may not be the exact issue that the buyer has.

With the exception of the last week of February, our inventory additions have been anemic. In every year but this year, inventory rises fairly steadily from the beginning of the year through May. This year, inventory actually fell in the first six weeks of the year from 86 listings at the beginning of 2025 to only 80 listings in the second week of February, when we once again set an all-time low of only 80 listings compared to 125 listings for the same week in 2024 and 532 listings in the same week in 2019.

Think about that for a second. In 2019, we had 532 single-family listings on the Greenwich MLS, or 6.25 listings for every listing that we have in 2025. Now, 2019 was not a good year for Greenwich real estate. Inventory was above average, and demand was below average. In 2019, despite having a surfeit of inventory, we only sold 526 houses. You had to go all the way back to 2009, at the bottom of the Great Recession, to have a lower number of sales. (OK, it was a really low 370 sales in 2009, but we were not looking good in 2019.)

Prices in backcountry, and to a lesser degree mid-country, had been falling for most of the 10 years post-2019. Big houses with lots of land, further from town and transportation, had fallen out of favor. Then came Covid. All of a sudden, panicked New Yorkers wanted lots of land for social distancing. They wanted bigger houses because they were living in them 24/7 rather than going out to plays and dinner every night. They wanted lots of amenities, both indoors and outdoors, giving rise to the term mini-country club.

The result was that we had the most sales ever in 2020 with 861 sales, only to see that number blown away in 2021 with our all-time record sales of 1006 home sales. Since then, our sales have been cut in half to only 500 sales last year, even below what we had in the “bad” year of 2019, with the aforementioned 526 sales.

While the year-end sales numbers were about the same, the markets in 2019 and 2024 could not have been more different. We had seen a multiple-year slide in demand going into 2019, resulting in fewer sales and a pile-up in inventory. In 2024, we saw a continued multi-year slide in listings as people were reluctant to put their houses on the market.

As I wrote several times last year, the lack of inventory in Greenwich is not due to a low interest mortgage “lock-in” effect of people not wanting to sell because they have low-interest mortgages. Our two biggest groups of buyers are downsizers who usually have lots of equity and don’t need a mortgage, and first-time buyers who don’t have a mortgage. Of course, higher interest rates do mean that some people decide a new house is too expensive at today’s rates, but it is not a lock-in effect for the large majority of Greenwich buyers.

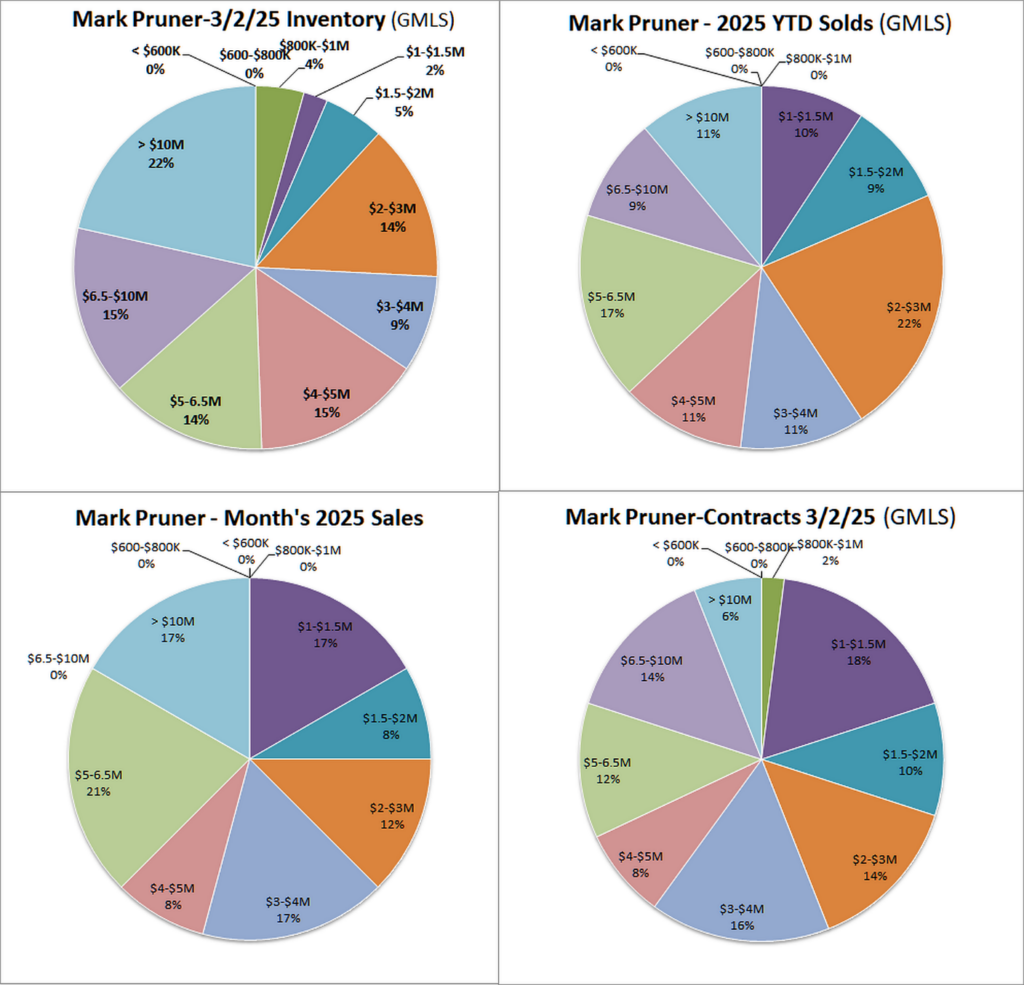

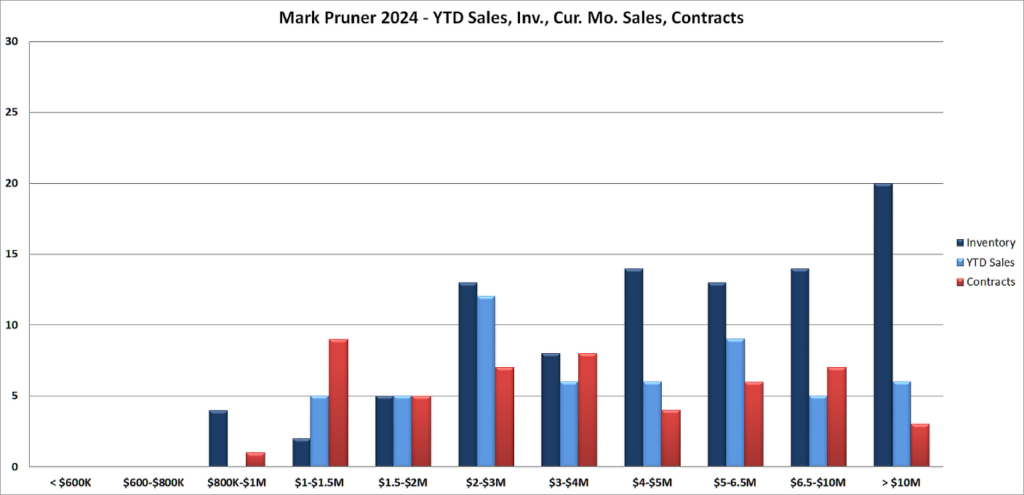

When you look at the market by price range, there is a distinct line at $4-5 million. Below that price range, sales and contracts are mostly down. The one exception is from $1-1.5 million, where we had some inventory come on and go quickly to contract. Sales are up by only one sale, but contracts are up by five, from nine contracts to 14 contracts, so that price segment will see an upswing in sales in March and April.

Above $5 million, sales are up 100% from 10 sales last year to 20 sales this year. Contracts are also up 60% from 10 contracts last year at this time to 16 contracts this year. This is because we have sufficient inventory and better demand this year.

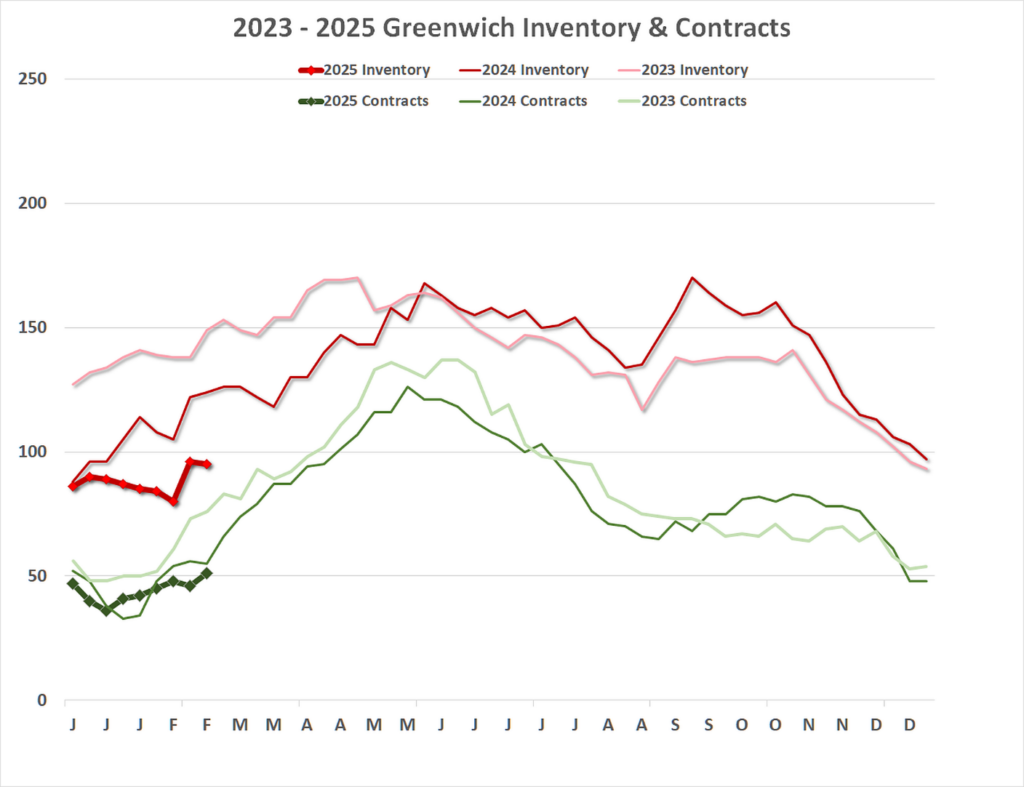

The question is, what are we going to see in the next few months? Our best forward indicator is signed contracts, which have risen since the beginning of the year as is typical in our late winter market. Higher contracts lead to higher sales in the next month or two. However, while contracts are rising, they are still below last year’s contract numbers at this time of year.

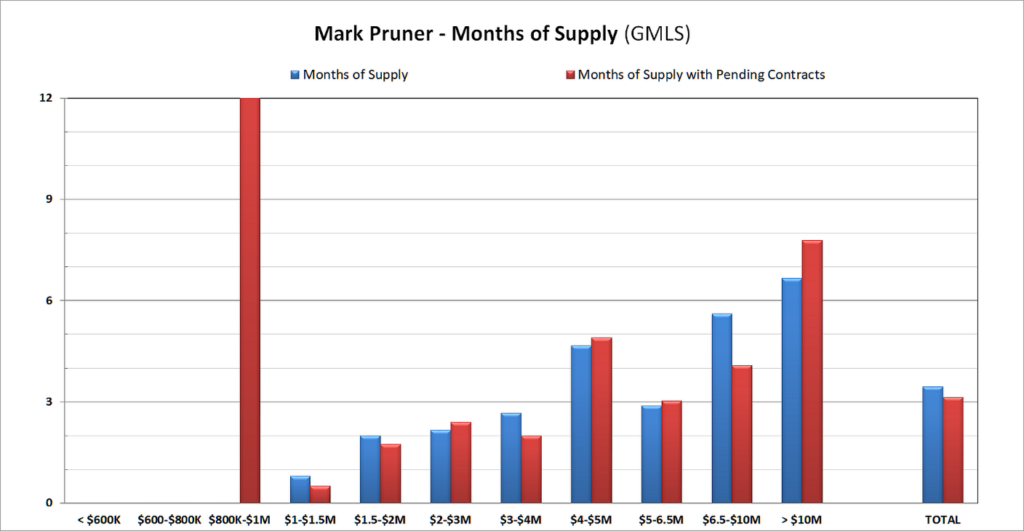

Arguably, inventory is rising slower than normal, but what is coming on is going to contract quickly, if it is a good property. The median days on market for the 25 sales in February was only 39 days from listing to non-contingent contract. Also, only six of the 25 sales had a mortgage contingency, i.e., the winning bidder in 75% of the deals brought cash.

The big question is, when are we going to see inventory rise above 2022 levels? There is a good chance that this may be the year. Inventory has been low for four years, which means many growing families are in houses that are too small for them, and downsizers are paying more than they need to for the amount of housing that they actually need. In Greenwich, much of our inventory comes from the natural lifecycle of homeowners: marriages, births, job transfers, graduations, retirement, and permanent departures. People need to move on with their lives, and they have changing housing needs.

Anyway, let’s hope this is the year. Stay tuned…