In times of economic uncertainty, transactions slow down, and closings are often the most affected. You would think that closings, whose closing dates are set out in a contract signed by buyer and seller, would show the least effect of economic fluctuations, but historically that is not the case. When the economic future becomes uncertain, people put off closings.

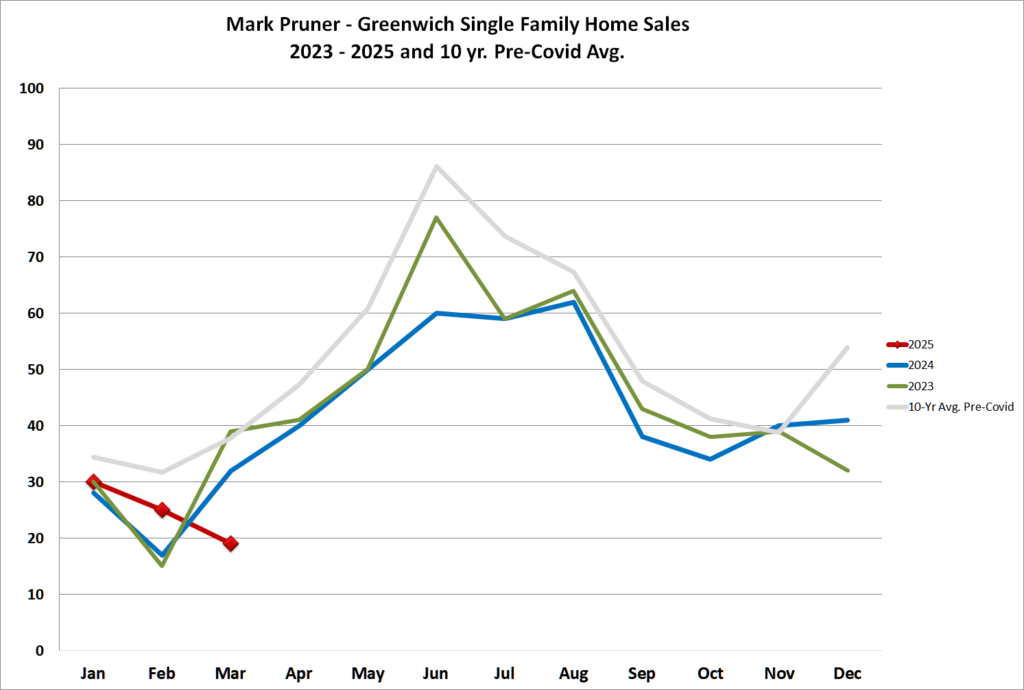

That is certainly what happened in March. In a month where our 10-year pre-Covid average in sales was 42, we didn’t come close. Even in March 2024, with only slightly higher inventory levels than we have now, we had 32 sales compared to this March’s 19 sales.

What we didn’t have in March 2024 were financial prognosticators raising the chances of a recession. In the last 25 years, only one March came close to having such a low number of sales, and that was during the worst part of the Great Recession in March 2018, when we had 18 sales.

So, does that mean that the Greenwich real estate market is as bad as it has ever been this century? Luckily, the answer is no. When times are uncertain, sales drop, but contracts are still rising as they do nearly every spring market. Contracts are our best forward-looking indicator and they show that deal are still getting done.

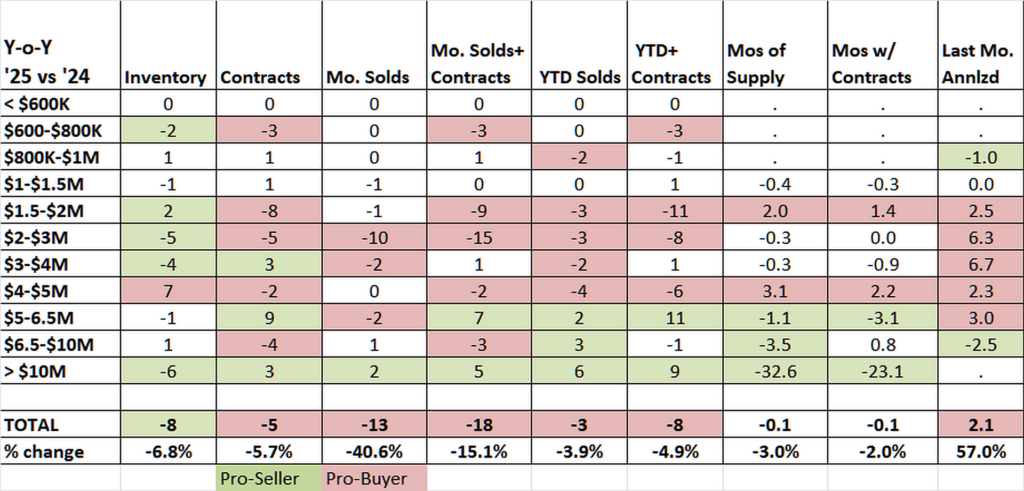

At the beginning of this April, we had 82 contracts, down only 5 contracts from the 87 we had at the beginning of April 2024. If only half of our contracts close in April, then we will have 41 sales, the same as we had in March 2024 and in March 2025. Based on this, we are not likely to see a repeat of the very low sales we saw last month.

If we delve deeper and look at the inventory and contracts by week, contracts look similar to a standard spring market with contracts accelerating in March, albeit slightly below where contracts were in March 2024, which were slightly below the number of contracts each week in March 2023. All this comes down to inventory.

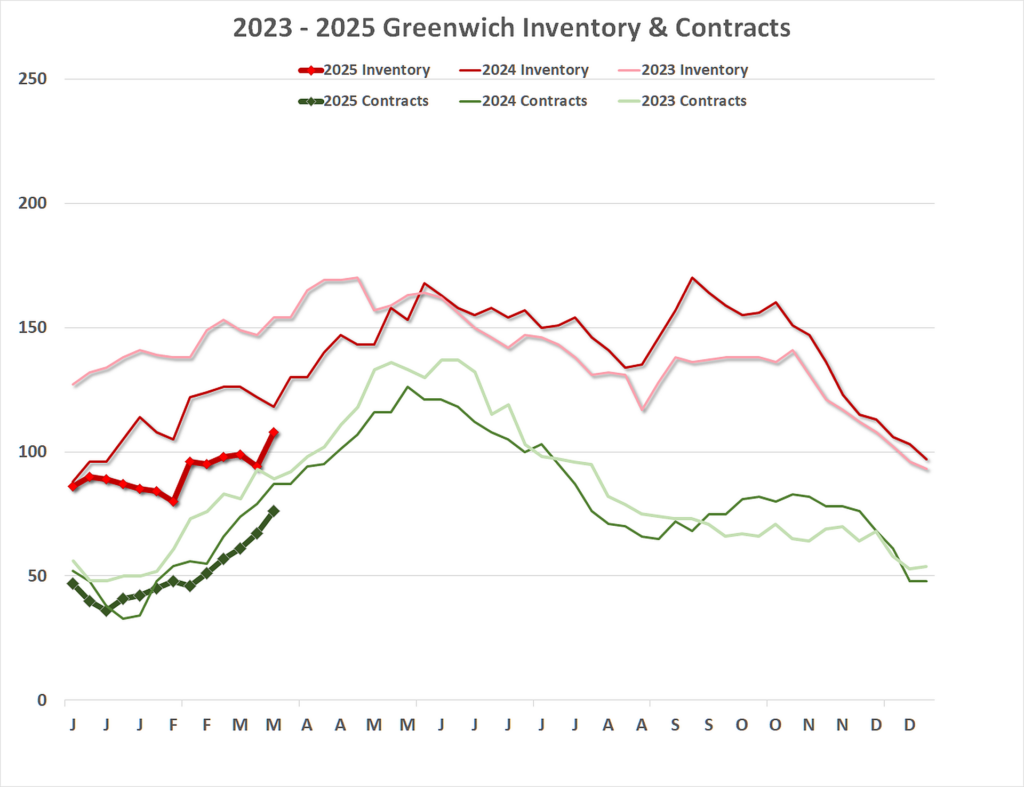

Inventory started to drop to unheard-of levels in the second half of 2021. In 2022, 2023, and 2024, we saw new and much lower inventory lines each succeeding year. As a result, sales were also a little lower each year, with 2024 having the lowest sales in 14 years. Then came 2025, and inventory got even stranger.

At least in 2023 and 2024, while inventory levels started at record lows, they went up as they always do. We didn’t see that this year. Inventory went down from what was already a record low opening inventory and declined for the first seven weeks of this year. That never happens. What we were seeing, and continue to see, is that anything decent that came on the market in 2024 went off as quickly as it came on, so inventory was staying flat.

To see this in action, take a look at Tim Agro’s table of sales last week. We had nine sales, and seven of those nine sales went to contract in 19 days or less. The other two sales were on the market for 140 and 167 days on market (DOM), which curiously is also a sign of a pro-seller market. In a tight market, you see houses that have been on the market for months sell because buyers have nothing else to buy, so they finally see the inner goodness that all the previous buyers did not.

The other interesting thing we saw in the weekly numbers is that the number of listings finally got over 100, finishing last week at 113 listings. Each of the last three weeks’ new listings have been in the double digits. This is what is supposed to happen in the spring market, but it is not what we had been seeing this year until March. The question this raises is if some of the financial smart money is putting their houses on the market now because they are expecting a softer market in the future. Only time will tell.

First quarter sales match last year almost

For the first quarter, we were seeing a pro-sellers market with smart, aggressive buyers. Of our 74 first-quarter sales, 36 of them went to non-contingent contract in less than a month. In addition, we had another 19 properties that went to contingent contract in less than a month. (For MLS days on market calculation, properties under a contingent contract are considered to still be “active” properties. These listings under a contingent contract continue to accumulate days on market until the contract becomes non-contingent.)

In total, 55 of our sales this year went to contract in less than a month. Also, only 27 of our sales had a contingency, meaning that if you wanted to win a deal, being ready to waive a mortgage contingency was a big help.

Of our 74 first-quarter sales, only 16 went for over list price, with another 12 sales going for full list price. This 38% of all sales going for full list or over list is down from what it was for all last year, but that is typical of the first quarter, where many of the sales were from listings that were over-wintering. Our median days on market was 54 for the first quarter, up from last year.

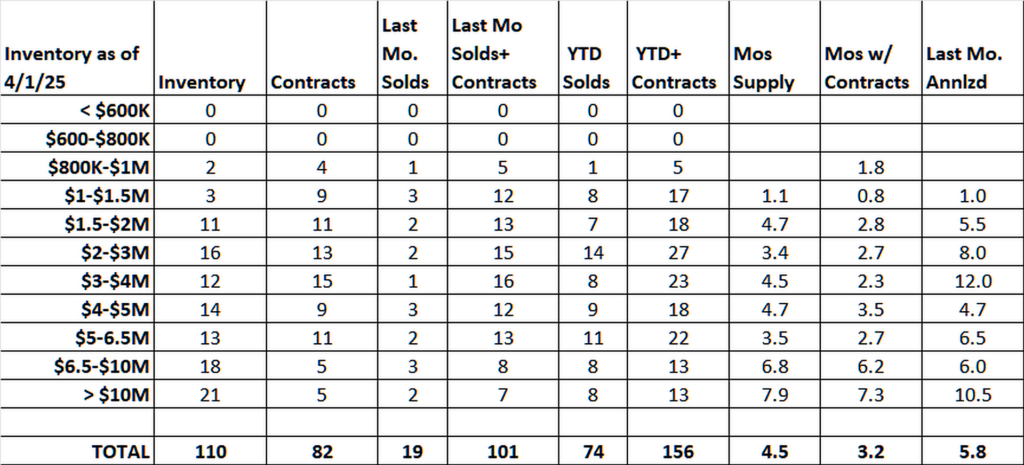

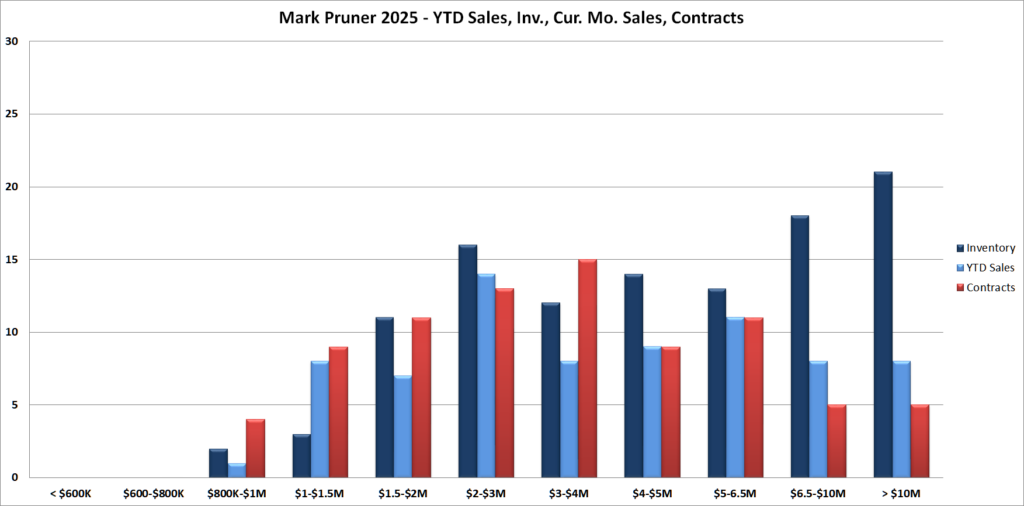

Price wise, the high-end is where the action is, with sales over $5 million up in 2025 compared to last year. Sales are down under $1 million because we have no inventory and hence no sales under $800,000 and only one sale from $800K to $1 million. Low inventory has also led to lower sales from $1.5 to $5 million compared to 2024.

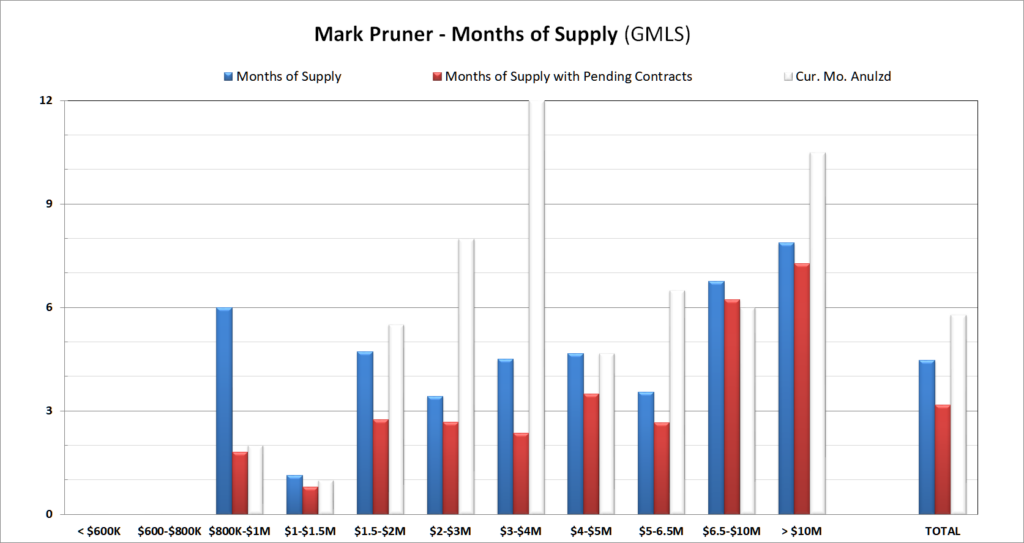

It is a sellers’ market below $6.5 million when you look at months of supply. However, if you take the slow sales in March and annualize them, it is only a sellers’ market under $2 million. As mentioned above, with the number of contracts, April should be a much better month for sales. Slow sales in March, even with lower inventory, mean current month annualized months of supply is seeing big jumps. Good contracts for the inventory we do have.

What about the rest of 2025?

What does all this mean for buyers and sellers in the Greenwich real estate market? The short answer is no one knows. The Greenwich real estate market is tied to the stock market, which did not have a good quarter. On the other hand, our inventory is so low that even if demand has dropped, we still have enough demand for the inventory that we do have. For those that have been waiting to sell, this may be a good time to list in case our some preliminary signs of softening grow.

For those looking to redeploy assets into a less volatile asset, Greenwich real estate is not a bad choice. For buyers who need mortgages, many have resigned themselves to mortgage rates in the 6–7 percent range, which still is historically low. Will we continue to see the price appreciation that we have seen over the last several years? That’s a harder question. If stocks are to trend lower, many of the stock investors tend to stay in stocks, just more conservative ones, so the influence on the Greenwich market is not huge enough to push up prices a lot.

Will house prices drop this year, like they have in places like Austin, Boise, and Orlando? This area has the lowest inventory percentage today compared to 2019. Even if we tripled our inventory, we’d still be well below historical averages. Demand could drop a lot, but would it be enough to see median prices actually go down? That is more of a stretch.

Stay tuned; it is going to be an interesting year.