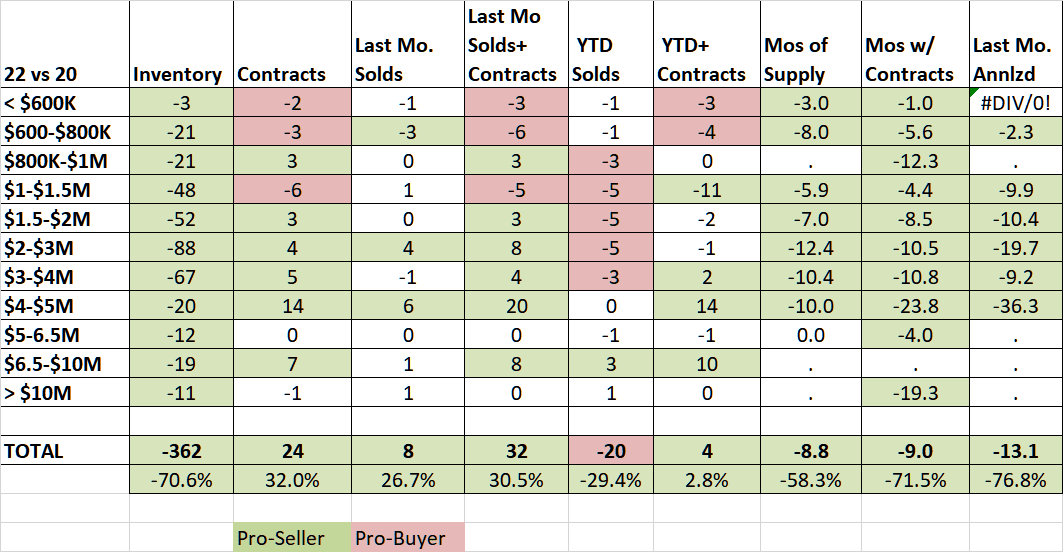

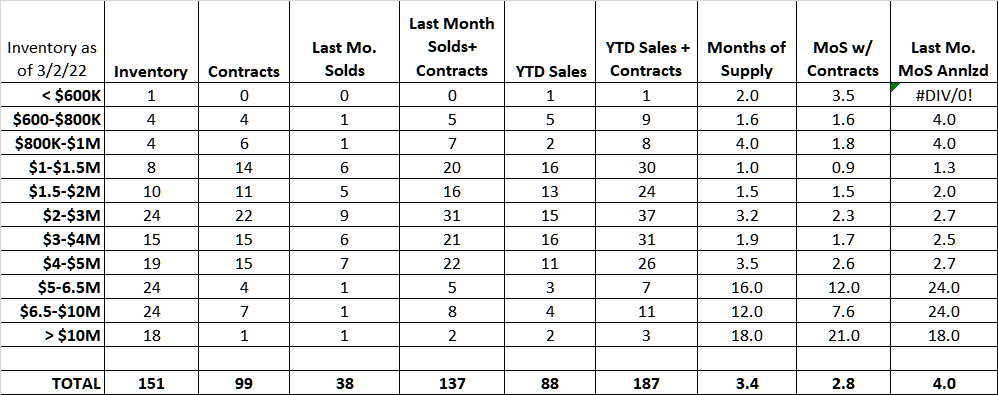

It’s not all that remarkable when contracts rise in the spring market. That’s what they’re supposed to do as more inventory comes on and buyers seeing the warm weather come out to buy houses. This year however rising contracts are actually pretty remarkable. Our inventory stands at only 151 listings. This is down 126 listings from February of 2021 and an amazing 362 listings from February of 2020, our last pre-COVID month.

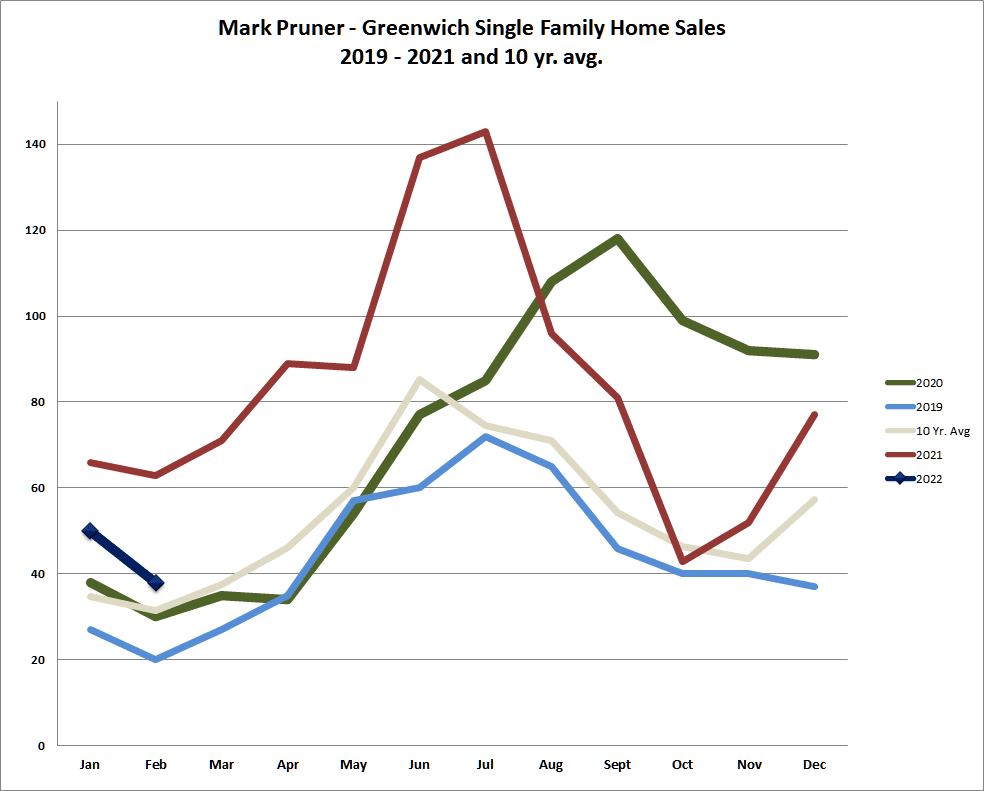

Even with our low inventory, February 2022 was an above average month for sales with 38 sales. Our 10-year average for sales in January, pre-COVID is 31 sales, so we were up 19% over our average February. For the pessimists, they can focus on year over year date. There our sales are down 40% from February 2021 and 32% for the first two months of the year. Now normally that would be considered a disastrous collapse of the market, however, those two months last year were record months with an amazing 129 sales in two months compared to our “paltry” 88 sales year to date.

When you look at a color-coded chart of sales, our inventory is very much pro-seller with inventory down in every category, except for under $600,000 where we have one listing this year compared to zero listings last year. In fact, however under $1,000,000 we only have 9 listings. The rest of the color-coded chart looks flat or very much pro-buyer with contracts and year to date sales down for the first two months of the year. Normally, that indicates a lack of demand, however in 2022, it indicates a lack of supply.

If you go back to February 2020, our last pre-Covid month, the world looks much different with most of the cells in green in a pro-seller market. Not only is inventory down a lot, but sales and contract are about evenly split up and down.

Russ and I recently put on a house just under $5 million that was in very nice shape and it had 24 showings in three days and multiple offers. It went to contract in 8 days from coming on the market. We are just really, really supply constrained; the buyers are out there.

Now this is not to say there, you shouldn’t worry about the market. If we don’t have any gas/inventory to keep the sales engine running, sales will continue to sputter, but probably not in March. The good news is our contracts are up significantly from last month, when we had 81 contracts, and now, we have 99 contracts. Our average sales in March are 38 houses, so with 99 contracts, we should be above average, but not near the 71 sales that we had in March 2021.

One thing to note however is that our inventory has been fairly flat for the first eight weeks of this year. What that means is that the new inventory coming on is matching our contracts. Having said that if we had more inventory, we certainly would have many more sales. This is the best time ever for a seller to put their house on the market and that’s true in every price range up to $10 million.

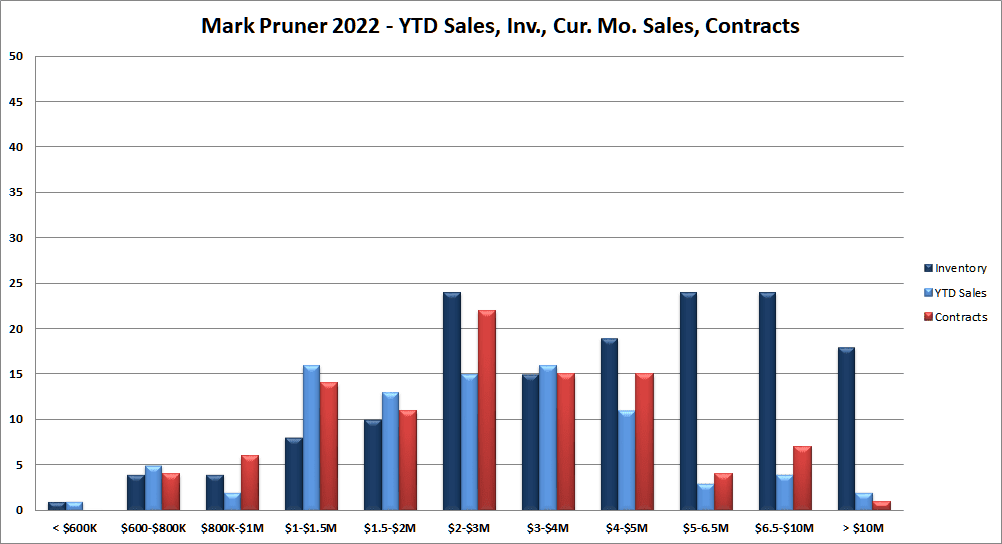

When you compare inventory to sales and contracts, we normally see a lot more inventory than we have sales or contracts. All the way up to $4 million, we actually have almost as many contracts and in some cases more contracts than we have inventory. It’s just a remarkable year.

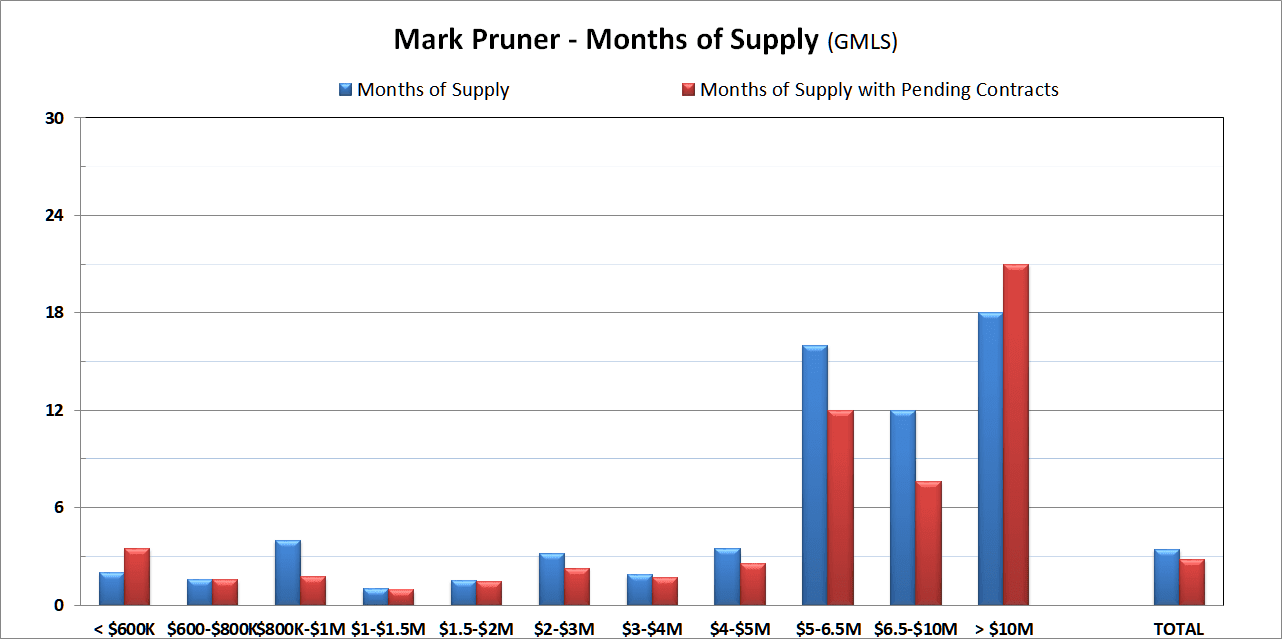

if you look just at sales, we do see a little weakness above $5 million where we have 24 months of supply from $5 – 6.5 million and 36 months of supply over $10 million. The thing to look at however is months of supply when you add in contracts and for all price categories that months of supply is going down indicating an accelerating market. For the market overall we have 3.4 months of supply and when you add in contracts we are looking at a ridiculous 2.8 months of supply.

The specter of rising interest rates is temporarily accelerating demand from buyers who need mortgages and who want to get in at the lower interest rates. We also are starting to see the return of the transferee market and companies are once again moving their senior people around the U.S. and bringing in people from overseas after a long hiatus. Last week, we saw buyers from London, Australia and Dallas.

Stay tuned the first quarter is going to be a very interesting period.