A Fast Car with Expensive Gas on a Stormy Night

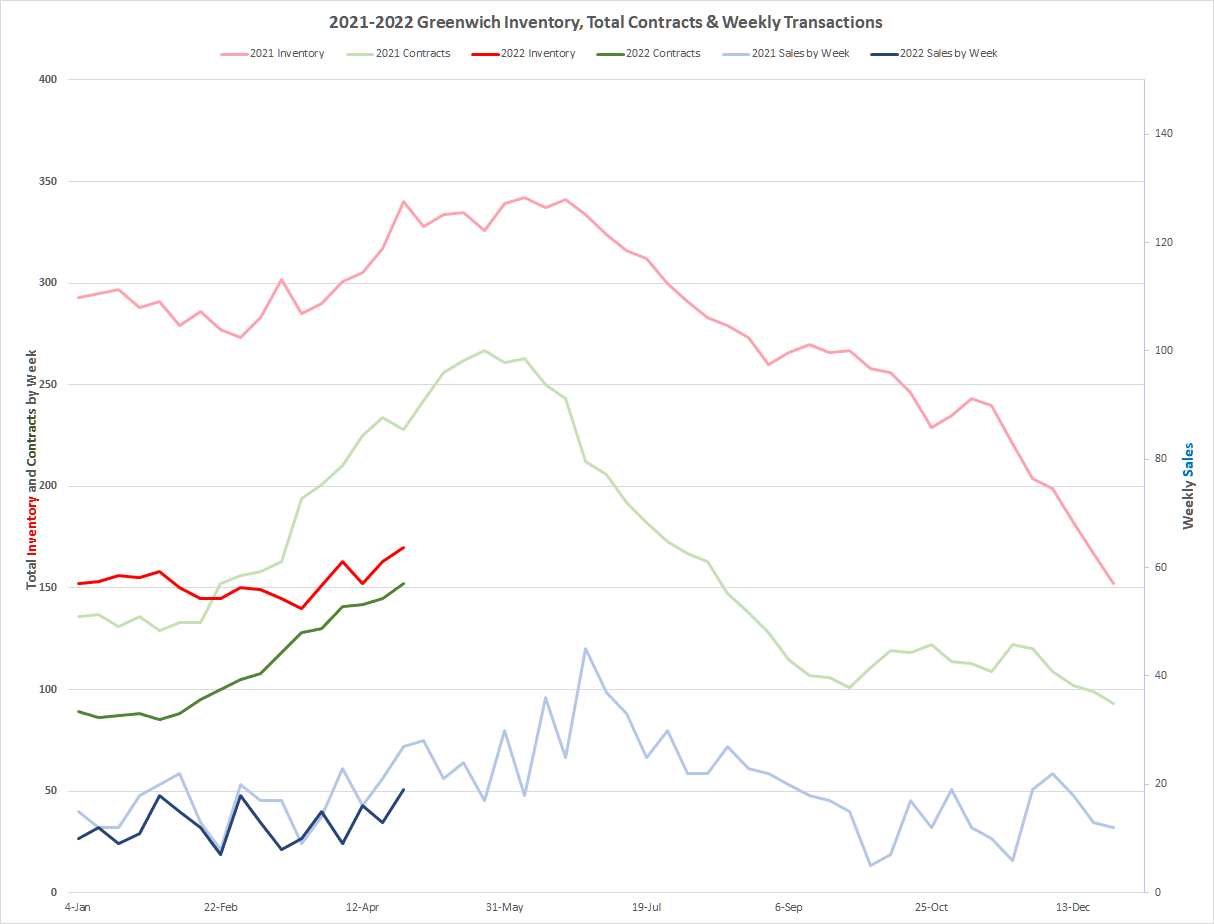

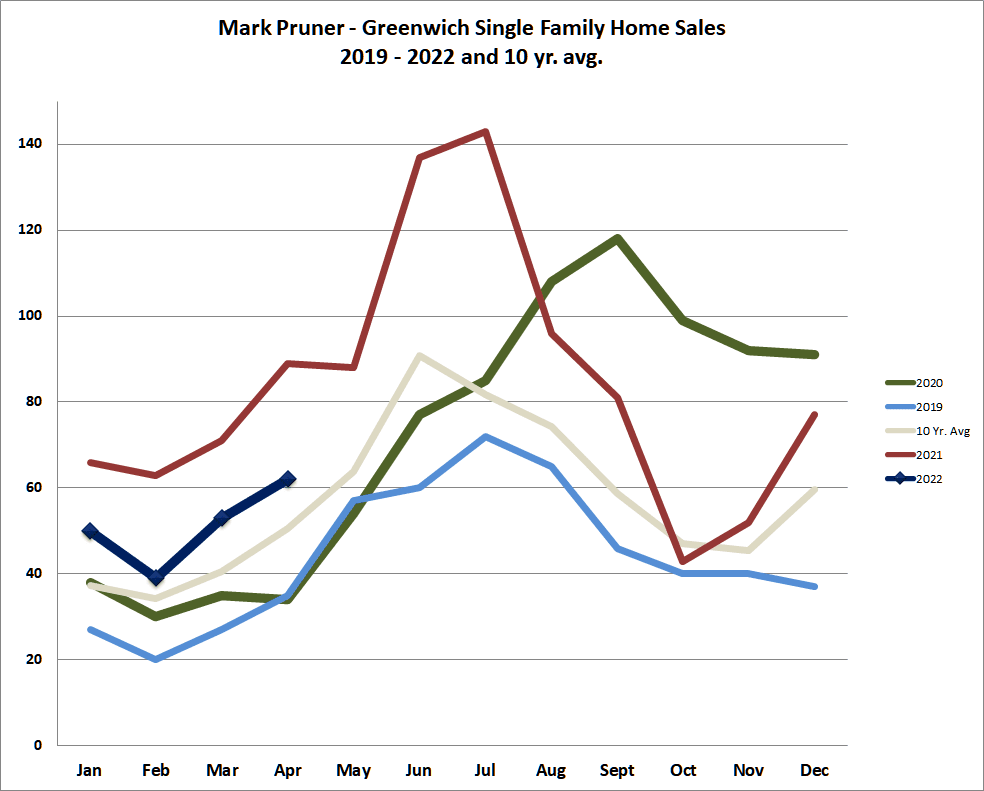

In April 2022, our sales were up 22% over our ten-year average. We had 62 single family home sales versus our ten average of 51 sales. At the same time, our sales were down 30% from last year’s all-time record April where there were 89 sales.

The remarkable thing is that the 62 sales happened at the time when we were experiencing record low inventory. On one day in early April our inventory slipped to 136 listings. Pre-Covid, the lowest inventory we ever had was 299 listings. Look at another way, our sales in the one month of April was nearly half of the listings on that date. However, that’s not the way it really works. Of our 62 sales in April 2022, only 8 of those sales went to contract in April; 54 of the sales were signed in March or earlier months. (One April sale went all the way back to a contract signed in June 2021. It was a foreclosure that took 11 months to get through the bank process. It shows why foreclosures often aren’t the deal they seem to be.)

By the end of April our inventory was up significantly for the first time this. year, but still not nearly enough to meet present demand. In the first quarter, we had been averaging around 150 listings before drifting down in early April to a weekly close of 140 listings. In the last two weeks inventory is up 21% to 170 listings a jump of 21% in only 3 weeks. One argument to be made here is that the smart-money homeowners are expecting that with the increasing interest rates that the market will cool, and they want to get their houses on the market, before the cooling becomes apparent. Or it could be just good weather that brought out more listings.

The good thing is that inventory is going up for whatever reason. This is also resulting in sales going up, but when you look at the slope of the curve, it’s not as steep as last year. Through April we have 204 sales this year versus 288 last year or a drop of 29% in sales.

Our contracts are down from 266 contracts last year to 152 as of the end of April this year or a drop of 43%. Contracts usually take 2 – 8 weeks to mature into sales, so don’t expect us to reach last year’s record sales in the next two months. Even if we have a substantial increase inventory it will take awhile before we see sales catching up to last year.

All this is like expecting that when Babe Ruth hit 60 home runs in 1927, that he was going to 73 home runs in 1928, since his 60 home runs in 1927 were 13 more than he hit the previous year. It’s just not going to happen. In 1928, he hit a still impressive 54 HR’s. Our 204 sales so far this year is almost twice the 109 sales we had in the first four months of 2019. If we can get the inventory, we’ll still have an impressive year, but it’s very unlikely, we’ll break the 1,000 sales mark like we did last year.

The price range beating 2021

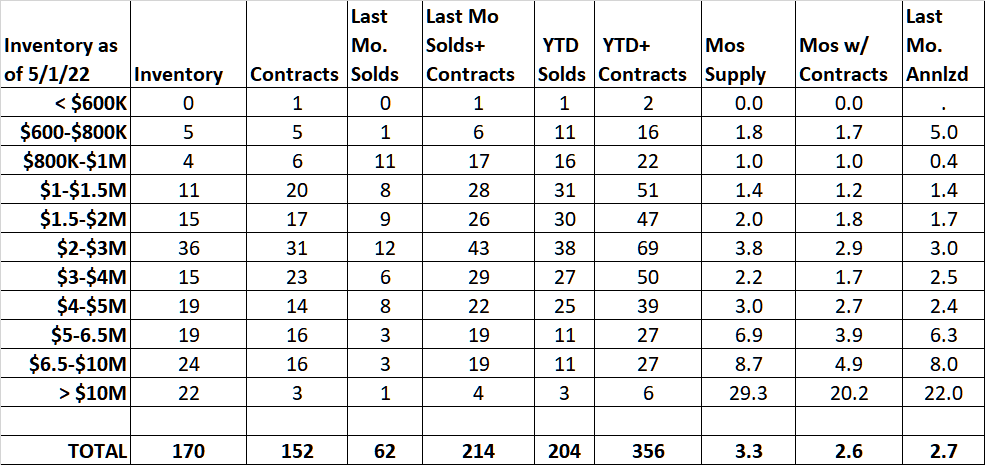

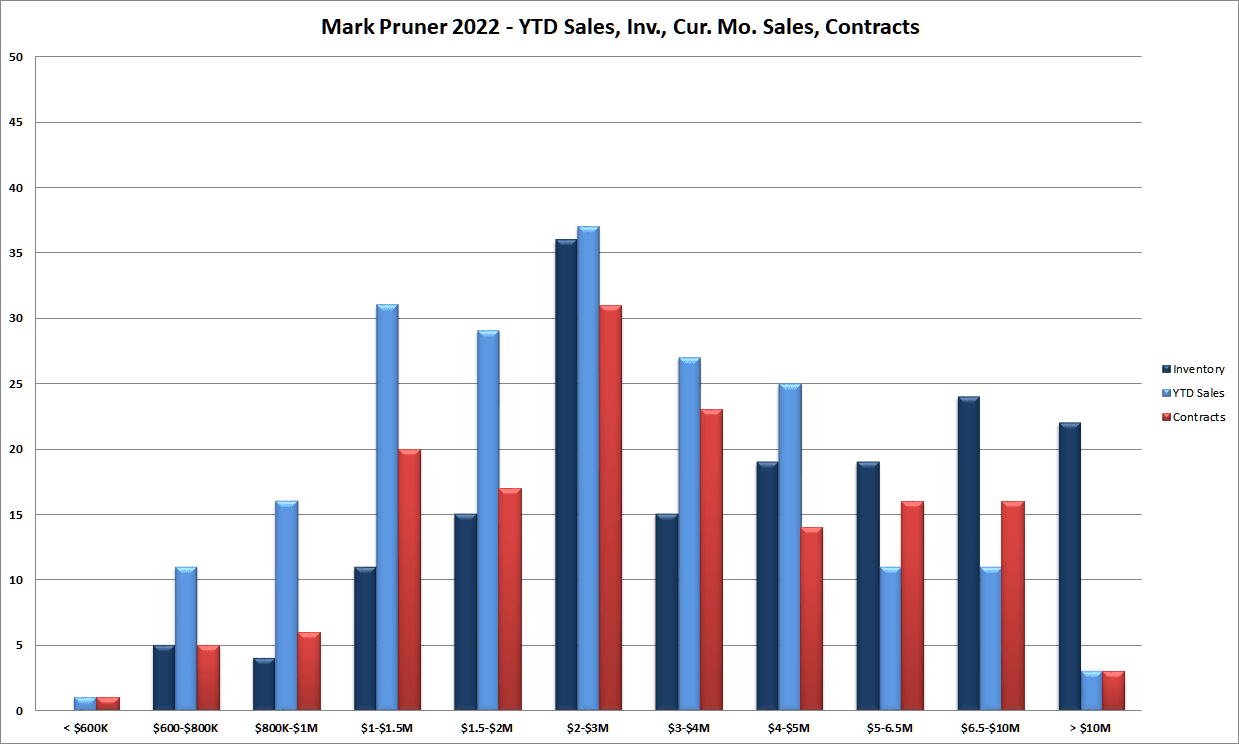

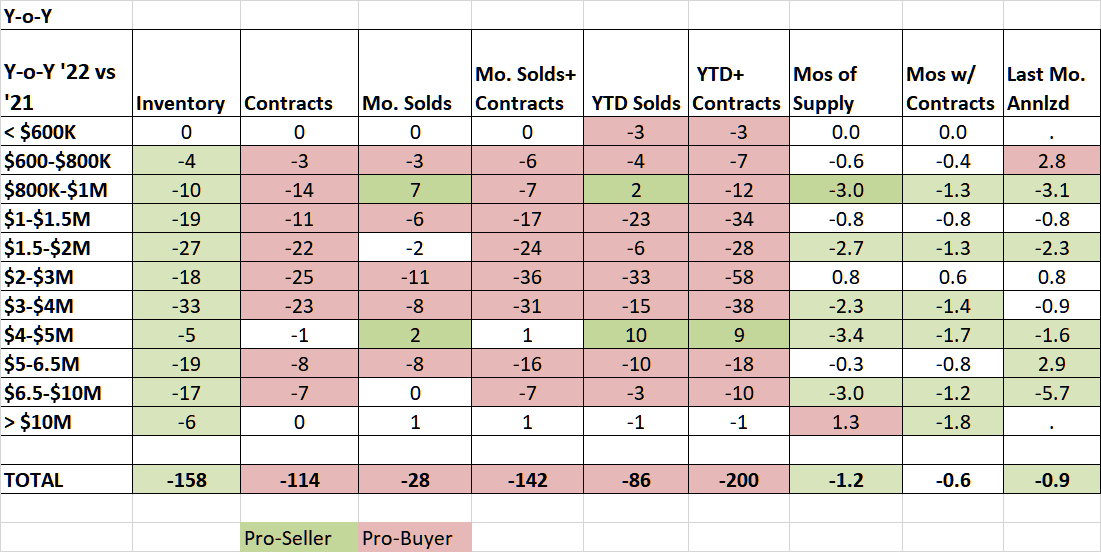

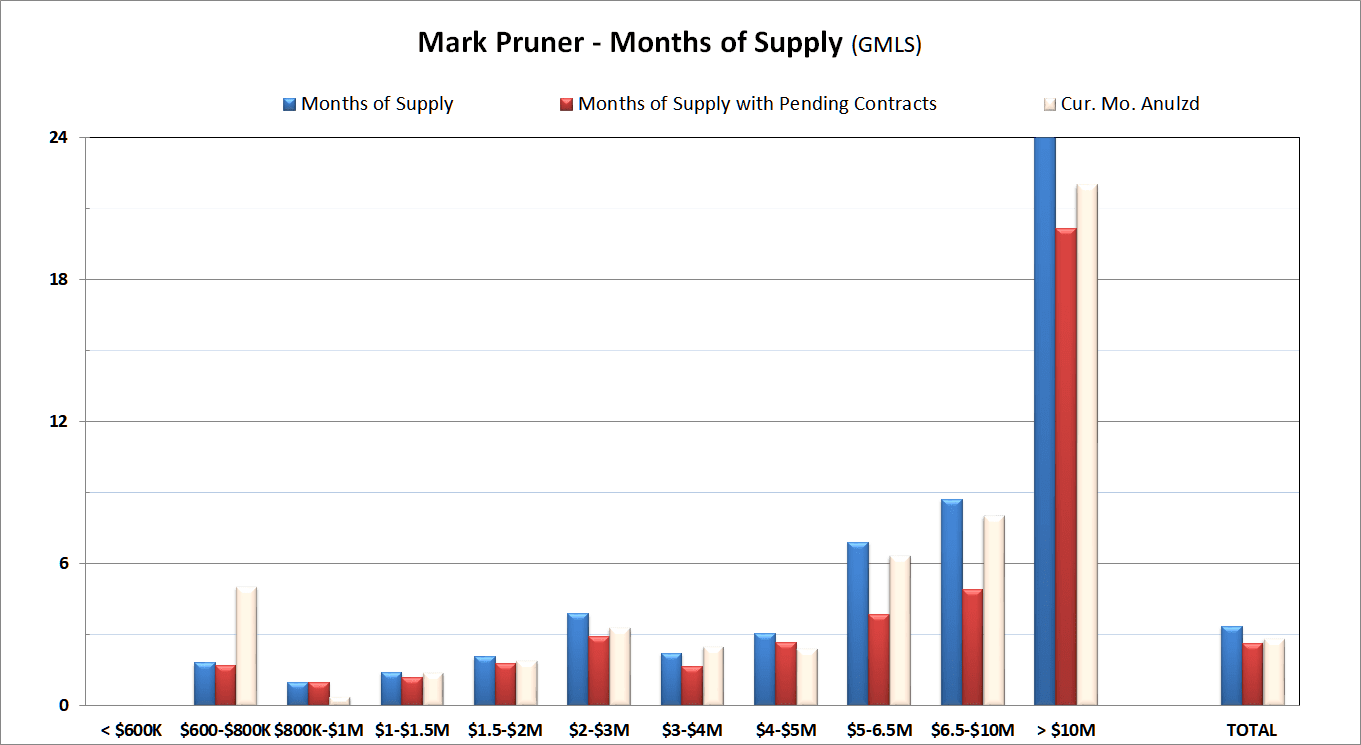

Every year there is some range or area of town that surprises you and this year it’s the $4 – 5 million price range. Sales there are up 67% from 15 sales last year to 25 sales this year. With 25 sales and only 19 listings in inventory you are looking at 3 months of supply. Add in the 14 contracts and months of supply drops to 2.7 months of supply. Annualize the 8 sales in April and you are down to 2.4 months of supply. When you see months of supply drop like this, it is a sign of an accelerating market, so if you have something to list in that price range, now is a good time to do that.

In fact, given that just about everything below $5 million has less than a 3-months supply, this is great time to list a house. It’s not till you get over $5 million that you see any sign of softness and that may not last. While we have about 8 months of supply from $5 – 10 million, if you throw in contracts, you are back down to a very pro-seller 4.5 months of supply. The one fly in the ointment is that April was a poor sales month for the $5 – 10 million sale bracket with a little over 8 months of supply when you annualize the six April sales against the 43 listings.

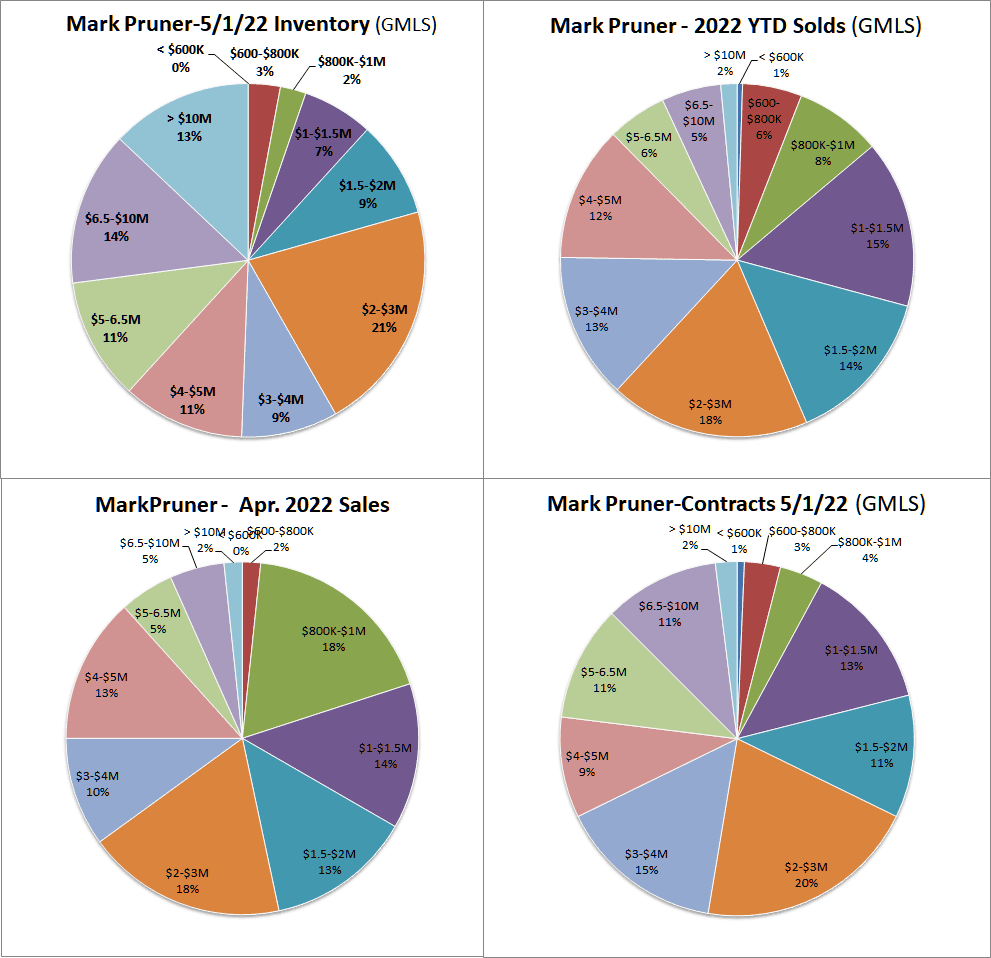

What this means is that we have way more sales (89 closings) than inventory (35 listings) up to $2 million. Above $5 million we have more listings (65) than we have sales (25). I wouldn’t however worry about this sector too much. Our high-end and ultra-high-end sales are now more oriented to 4th quarter sales as most of our financial folks no longer get one very big bonus in January or February which used to drive our first quarter high-end sales.

Another way to look at our market is that under our inventory under $1 million in only 5% of inventory and but represents 20% of sales. Our listings over $6.5 million account for 27% of inventory and 7% of sales, (but be patient with the high-end, it’s likely to look much better by December.

What’s Going to Happen for the Rest of the Year?

It looks like we will finish this year with 549 sales down from our 10-year average of 621 sales. Inventory will recover throughout the year and climb back to around 400 listings by year end. Demand will continue strong but tapering throughout the year. We will see a pause in contracts in October as people await the election results followed by a rebound in November with a strong December. (NB: THIS IS NOT GOING TO HAPPEN!). Anyone who says they know what is going to happen to the Greenwich real estate market this year, doesn’t know the market and if you do know the market, you can be sure you don’t know what is going to happen, but let’s look at some factors that will be shaping the market this year.

Rising Interest Rates

With the Feds announcement this week of a 0.5% increase in the fed funds rate and more to more to come demand should soften, but will it drastically cut into sales? First most people in Greenwich don’t have a mortgage contingency in their purchase contracts. This doesn’t mean that some of these buyers aren’t getting a mortgage, just that they are comfortable without having a contingency. So, will increasing rates affect the Greenwich market, some, but I expect the demand will continue to be high.

One aspect of this we are just starting to see is that homeowners with low interest rate mortgages may be more reluctant to put their houses on the market as they would have to give up a low interest rate mortgage for a high-interest rate mortgage and a higher cost per s.f. for a new house. Once again, though, if you don’t have a mortgage, this is much less of a factor. Mortgage interest deductibility is now limited to the first $750,000, so they are now a lesser factor and becoming even less of a factor as houses appreciate even more.

Shrinking Stimulus Here, Expanding It There

What is likely to affect the market is the disappearance of the Covid stimulus money. You take a couple of trillion dollars of stimulus money out of the market and inflation is likely to go down. But we have another major stimulus in the trillion dollar plus infrastructure bill. This at a time when construction workers of all types are in short supply. The infrastructure spending is spread out over five years, so the feds aren’t pumping a trillion dollars plus into construction this year, but it is going where it is likely to be a factor in pushing up housing construction costs.

International Issues

Shortages of all types and bottlenecks are likely to get better, but foodstuff shortages will continue to increase as the Ukraine war cuts into exports from two of our largest exporters of grains and oil. These are ingredients in much of the food that we eat. China with it’s Covid zero policy is also likely to continue exacerbate shortages as factories continue to shut down, but don’t forget it’s an election year for President Xi also.

Work from Home

Even as Covid recedes or maybe better said, as the impact of Covid recedes, with vaccines, better medicines and better treatment, you are not going force people back to Paree offices full time, once they’ve seen life on the Greenwich homestead. I’m guessing we have a couple of years, before the new office/home work balance finally settled into some form of homeostasis. With less time spent commuting a Greenwich home looks more inviting and will for a couple of years.

List Now or Later or Stay Put?

It’s been an interesting week as three Greenwich homeowners in the finance industry have called me up to pick my brain about what they are thinking of doing. I love these conversations, as I learn as much, or more, than they do. (So, if you are wondering what to do please feel free to give me a call. I’d love to hear your thoughts.)

There is a genuine concern about a recession, but we all agreed it’s probably less than 50%. The big issue seems to be just how long it takes for higher interest rates to really affect the economy. Most of the time when the Fed does serious tightening it leads to a recession. The Fed often continues to tighten too long leading to recession. Let’s hope they learned their lesson and the Internet, and the faster flow of information means they are more nimble this time.

The thought last year for many people who decided stay in their house was that their Greenwich house was only going to be more valuable, and it is. While this is likely to happen again this year, it’s not as certain as it was. You have the issue of a possible recession, and you also have high inflation, so the price may go up, but your real return is less.

TINA is also dying. For much of the last decade of ultra-low interest rates, investor said There Is No Alternative to the equity market. With interest rates were so low and houses not appreciating much, keeping your money in equities didn’t looks so bad. Now, interest rates are going up, bonds are falling and so is the stock market as money is moving to the improving and lower risk returns in the bond market. The 2022 question is are you going to get your best return in stocks, bonds or Greenwich real estate?

The one thing we do know is that right now, our inventory is way down and we have lots of demand at least up to $5 million. Properly priced, your house should sell quickly, but there all those other issues too.

Stay tuned it’s going to be an interesting year.