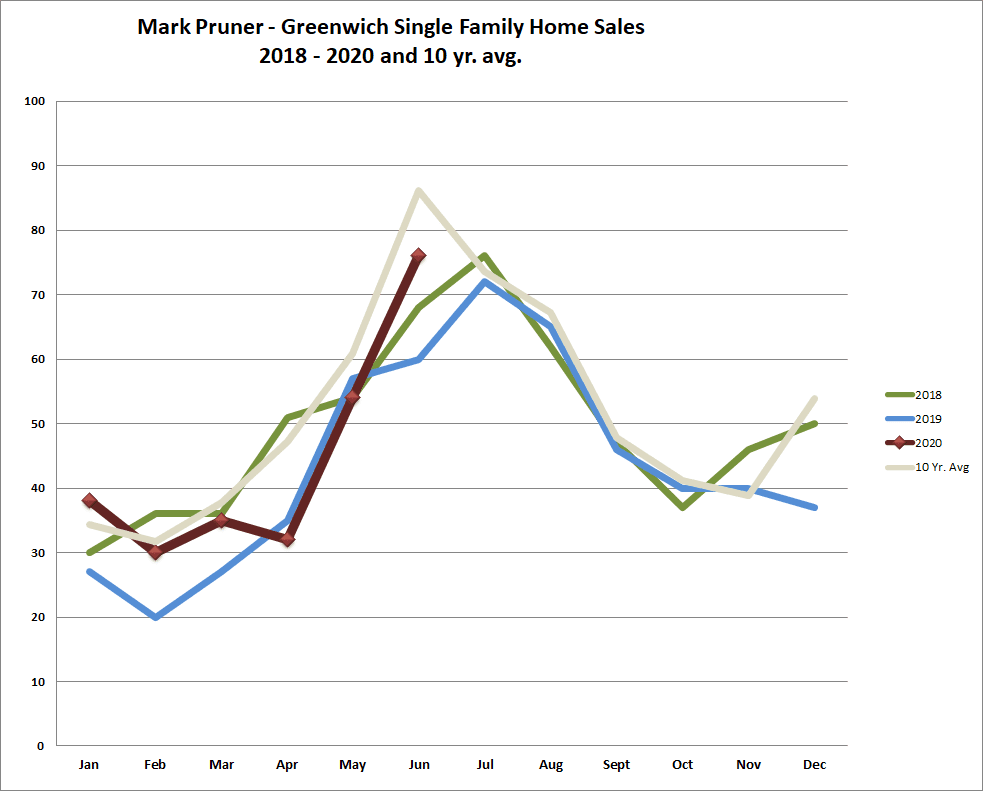

This week we start with a quick update on June sales and how June went out like a lion, which given that we are now in our Covid time-shifted spring market is a little to be expected. The rest of the article is look at how our neighborhoods did in the first half of the year.

June Sales Update

If you could take one day of the year and clone it for the rest of the year, that date would be June 30, 2020. On that date we sold 12 houses out of 76 sales for the whole month of June. Of those 12 sales, the average price was $5.93 million. A house at 49 Midwood Road sold for $10,750,000 after 435 days on the market and a house at 45 Field Point Circle sold for $12,800,000 after 220 days on the market. In addition, we had sales of $7,500,000, $4,995,000 and $4,200,000 all on June 30th. As I wrote last week, the July 1st increase of 1% in the state conveyance tax for sales over $2.5 million was the motivated factor to get all these high-end deals done before the new tax kicked in.

But let’s get back to those 76 total sales for the whole month, that number is well above the 60 sales we had in June 2019 and even 4 sales above what we had in June 2018 when we didn’t’ have a pandemic. We also have 171 contracts waiting to close which is up 68 houses from last year or a 66% jump from last year. We are doing better in just about every neighborhood, but three neighborhoods are seeing some headwinds.

The last time the conveyance tax was raised in 2011 we saw our biggest sales month ever with 114 sales in June 2011, followed by our worst July with only 48 sales. We won’t see that this July as we have just too many contracts waiting to close.

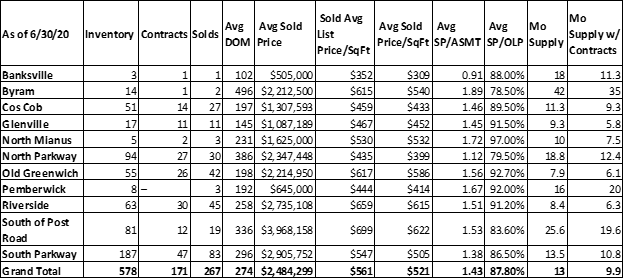

The 2020 First Half Greenwich Neighborhoods Report

The Tight Neighborhoods

Glenville

When you look at months of supply the neighborhood that really stands out is Glenville and not so much for its 11 sales, but for its 11 contracts waiting to close for a total of 22 transactions. When you throw in only 17 listing with these 22 transactions you get a tight 5.8 months of supply with contracts which is the best in town. This is down 11.7 months of supply from last year. A lot of that drop is attributable to the number listings going from 28 house listings at the end of June last year to only 17 listings left this month. Tight markets don’t just happen, smart agents and sellers help. While we have a tight market the average list price in Glenville has dropped from $1.13M to $1.09 as sellers are more competitively pricing their listings.

Old Greenwich & Riverside

Last year I sold a house in Riverside to a developer and had another listing cancelled for lack of buyer interest. Riverside was a tough place to sell in 2019 which is unusual. This year Riverside is back and once again running neck and neck with Old Greenwich, a perennial favorite of buyers. Even in a time when people are looking for more space and larger houses, the village of Old Greenwich continues to attract buyers. One factor is the R-7 zone in both Riverside and Old Greenwich, which is mostly north of the Post Road, are smaller lots, but they look good to a family living in a small 2 bedroom apartment in NYC. Inventory is down for these two contiguous neighborhoods by a total of 49 listings to a total of only 118 listings. The average sale price is down in Old Greenwich, but took a big jump in Riverside up by $792K. Anytime you see a change like this, a large part is because of the mix of what is selling. Higher end houses with more space and more land are selling in Riverside, but we are also seeing higher sales price/sf a better indicator of an overall market move.

The Rapidly Changing Neighborhoods

Backcountry & Mid-Country

Last year we saw sales jump 30% in backcountry Greenwich and also go up in mid-country (which for GMLS data purposes goes all the way down to the Post Road). This year that trend is continuing. Mid-country is the new sweet spot in Greenwich with sales up 20 houses from last year and contracts up by 47 houses while inventory is down by 52 houses to only 187 listings. The average price, average price/sf and sales price to assessment ratio are all down, as motivated sellers are covering their bases just in case we do see a depression next year when their values might drop. While the stock market is at record levels and is not predicting a depression, it’s a good time for sellers to take some of their chips off the table.

In backcountry, sales are up 4 houses, but contracts are up 27 and listings are down 31. The result of all that is when you look at months of supply with contracts you only get 12.4 months of supply. Even if you just look at the actual sales months of supply, that is down 10.4 months from last year. People want land and houses with amenities; backcountry is one of the best places to get that.

Cos Cob

Cos Cob has seen a strong rebound after being our neighborhood with the poorest results in 2019. Now 2019 results looked down in Cos Cob, because it had done so well in 2016-2018. In 2020, Cos Cob is back like those prior years. Sales are up 10 houses and contracts are up 14 houses while inventory is down 10. This result in a competitive 9.3 months of supply. On the sales only side, months of supply is down 10.2 months of supply from last year to 11. 3 months of supply.

Higher Density Neighborhoods

Byram, Pemberwick and North Mianus have seen the greatest appreciation since the Tax Assessor last did a revaluation in 2015. Byram is actually up 33% from 2015 when you compare the sales price to the assessment ratio. Pemberwick is up 18% from 2015 when you look at the same assessment ratio. Lots of folks want to live in Greenwich and those are our most affordable areas. This year a combination of all this prior appreciation and a desire for more social distancing have made these three neighborhoods slower this year than last year.

In Byram, we have 14 listings and only 2 sales so far this year. In Pemberwick it is 8 listings and no sales. North Mianus was our hottest neighborhood last year, but this year months of supply are up 3 months from last years to 10 months of supply. If you throw in the 2 contracts pending and only 5 listings its drops to a very active 7.5 months of supply, it’s just not as hot as last year.

All three of these neighborhoods are small so a few sales would change things dramatically, but it is a little strange that these lower priced areas have not done as well so far this year, since the R-7 zones in Old Greenwich and Riverside are doing well.

Summary

For the town overall, inventory is down 20% and this is true across most every neighborhood. Sales are up 18% and once again this is widespread with big jumps in Cos Cob, Riverside, and mid-country. The really dramatic change is in contracts which are up 66% as this market is just getting hotter. The areas that are hot right now based on contracts are backcountry, mid-country, Riverside and Old Greenwich. As I write this, I’m negotiating three deals, two in backcountry and one in mid-country. Trying to find good listings in those areas is tough and if you are looking to sell now is a good time to list.