Greenwich Real Estate 2022 Year-End Report - 1/4/23

Mark Pruner | January 3, 2023

Mark Pruner | January 3, 2023

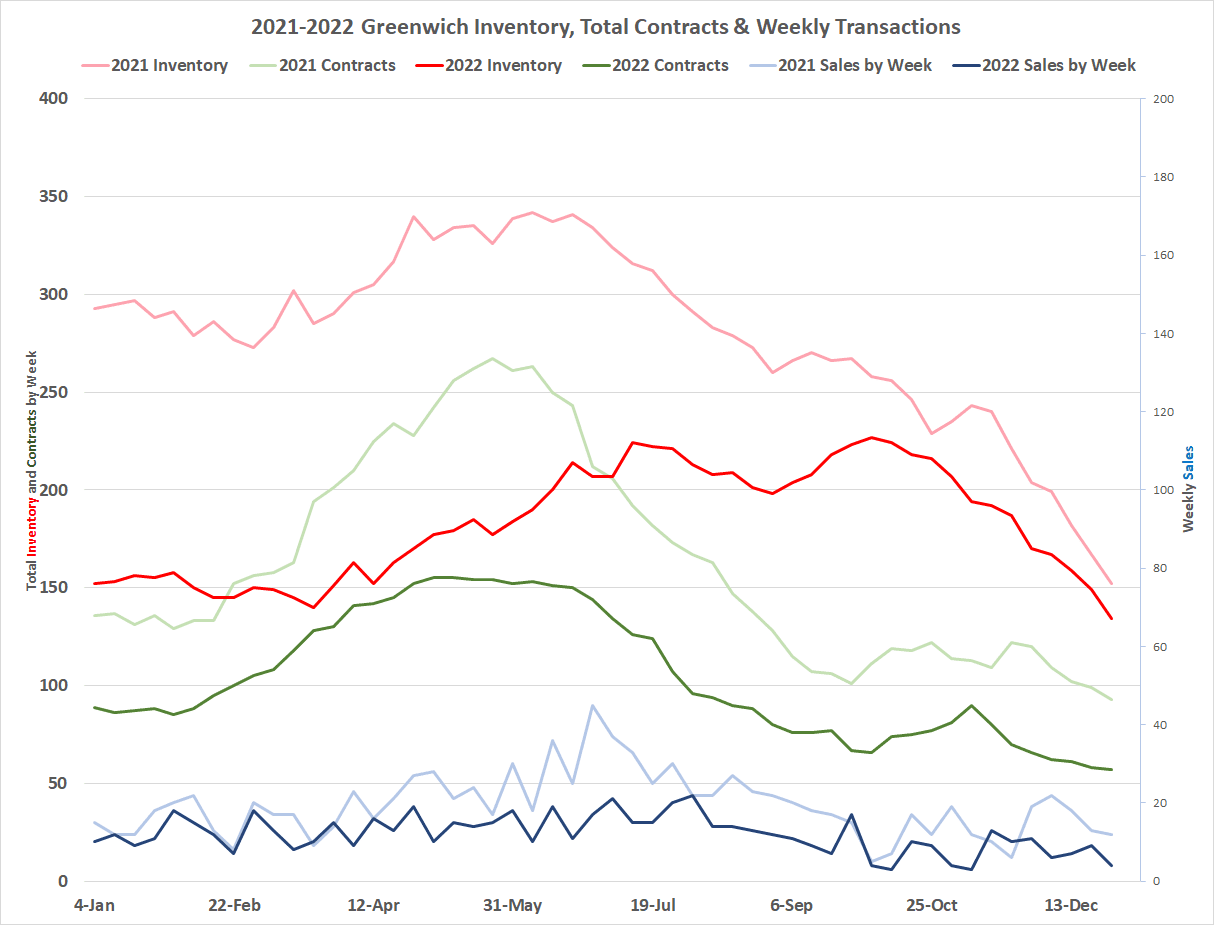

The Greenwich real estate market had an “average” year in 2022. That’s if you consider a wild roller coaster ride of big ups and downs with surprising twists and turns a normal year. The year was “normal” only because at the end of the roller coaster ride, we end up back where we started with a ridiculously low inventtory. In 2022, started the year with 152 single family home listings and ended the year with 145 listings. At the end there was a only a small drop in inventory from the beginning to December 31, 2022.

Of course, by the following day, January 1, 2023, another 11 listings had gone poof as many listings expired at year-end. We started 2023 with the lowest number of listings ever on the Greenwich MLS. Pre-Covid you have to go back to December 1991 for our previous low of 291. (This according to my brother Russ, who was there. Statistics are a family tradition. :). So right now our inventory is so low that it is less than half of our previous low, a number that had stood for 30 years as the lowest of the lows.

The average the number of listings at year end over the last 10 years once again according to my brother, Russ, who has statistics back to 1986 is 480 listings. Inventory is the lifeblood of our market, and we were very anemic all year. The highest our inventory ever got in 2022 was 227 listing in the middle of October. If you go back to our last pre-Covid year, 2019, that year we peaked at 795 listings, i.e., our highest number of listings for 2022 was a quarter of the highest inventory that we had in 2019. Our high for the year of 227 listing, was 64 listings below our previous low in 1991. We are far from average.

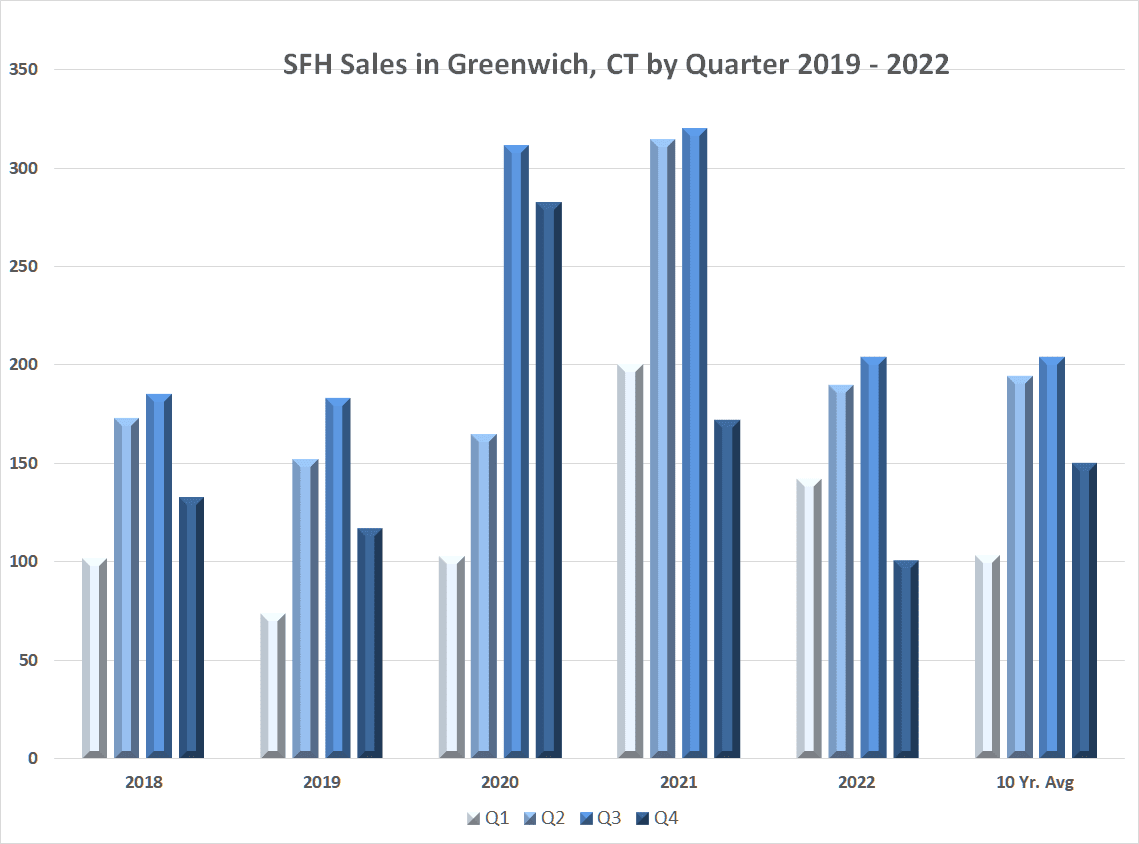

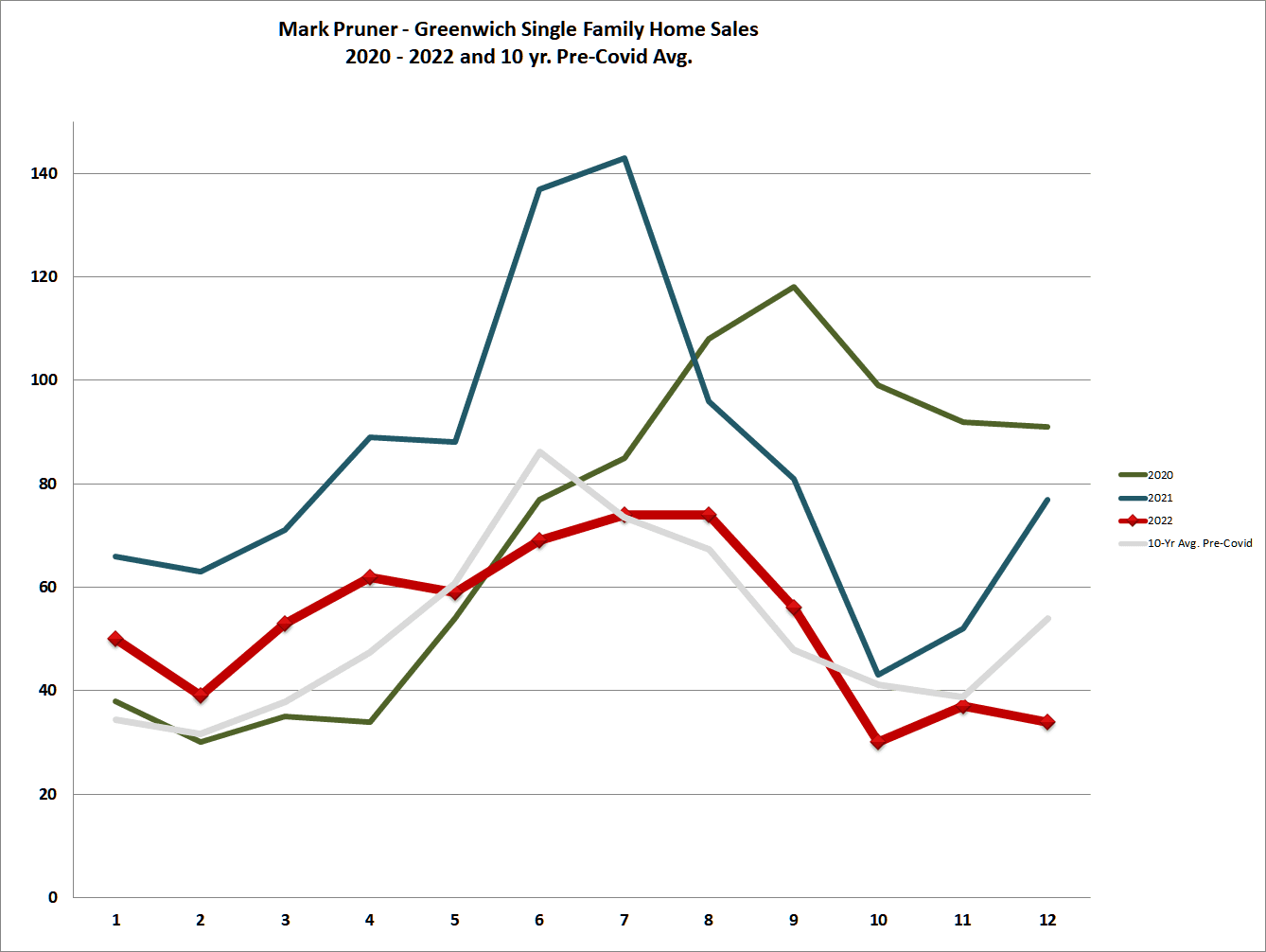

Given our record low inventory for every week last year, for us to get to 637 single family home sales in 2022 was remarkable. When you look at our sales quarter by quarter you can see what happened. We had a good first quarter with 142 sales compared to our 10-year average of 104 sales. The second and third quarters were almost exactly equal to our 10-year averages and then came the higher interest rates and stock market losses of the fourth quarter. In our fourth quarter, we had only 103 sales down from our 10-year average of 150 fourth quarter sales.

Of course, if you are really into self-flagellation, which a surprising number of pundits seem to be, you can compare our 2022 sales to our all-time record sales of 2021. If you do that every quarter in 2022 was a dramatic drop from 2021’s 1,006 sales. Or course, this is kind like comparing the 1969 Mets, with then Greenwich resident Tom Seaver, who won the World Series to the 1962 Mets with Craig Anderson who won only 40 games. Year-over-year comparisons can be deceptive, when you are comparing to records.

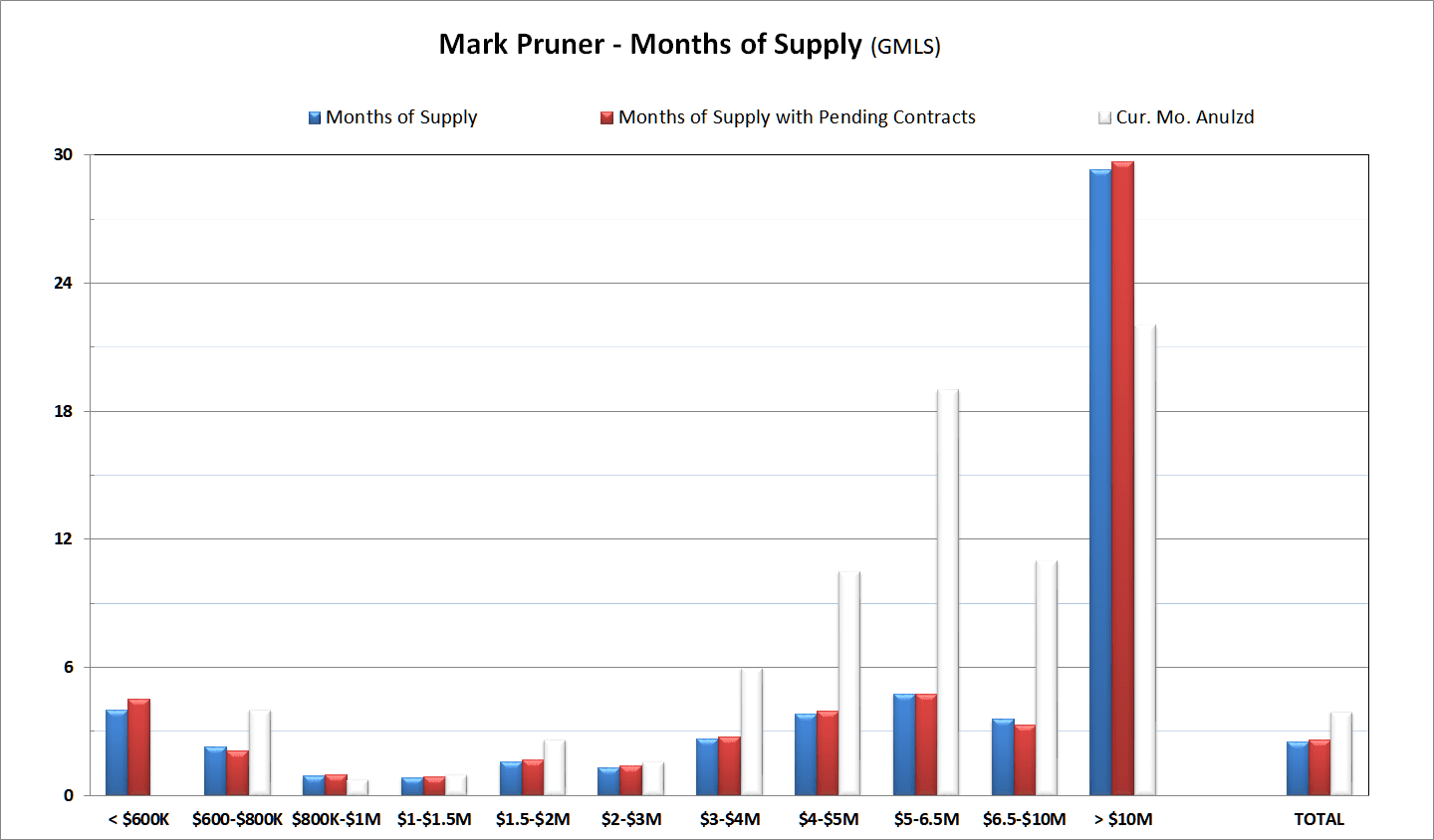

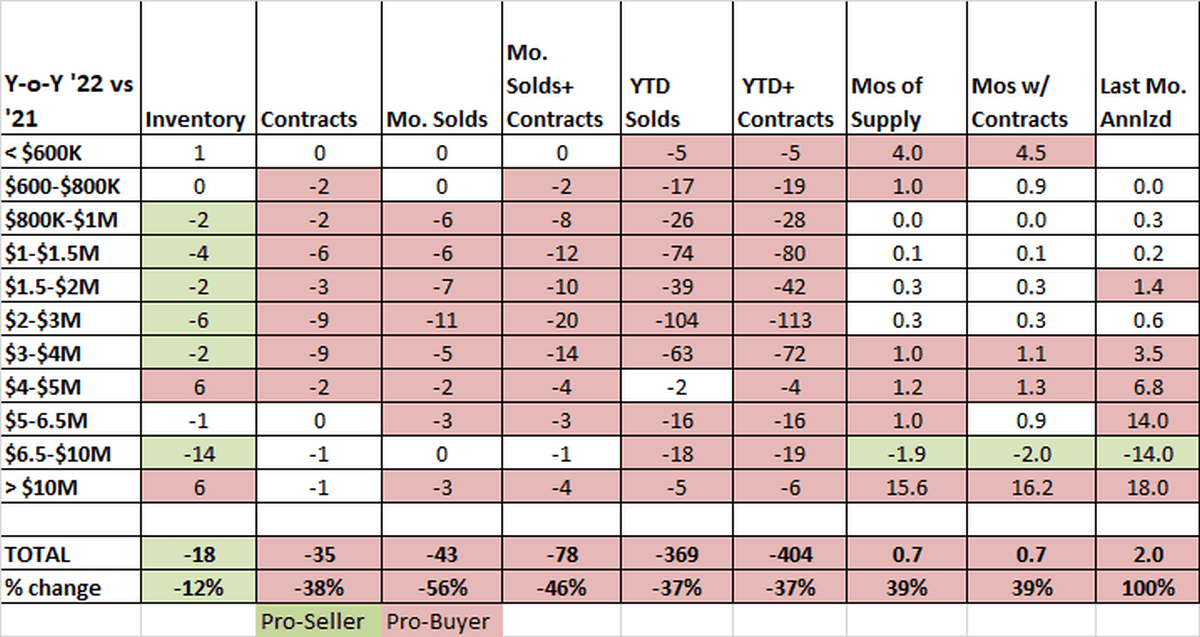

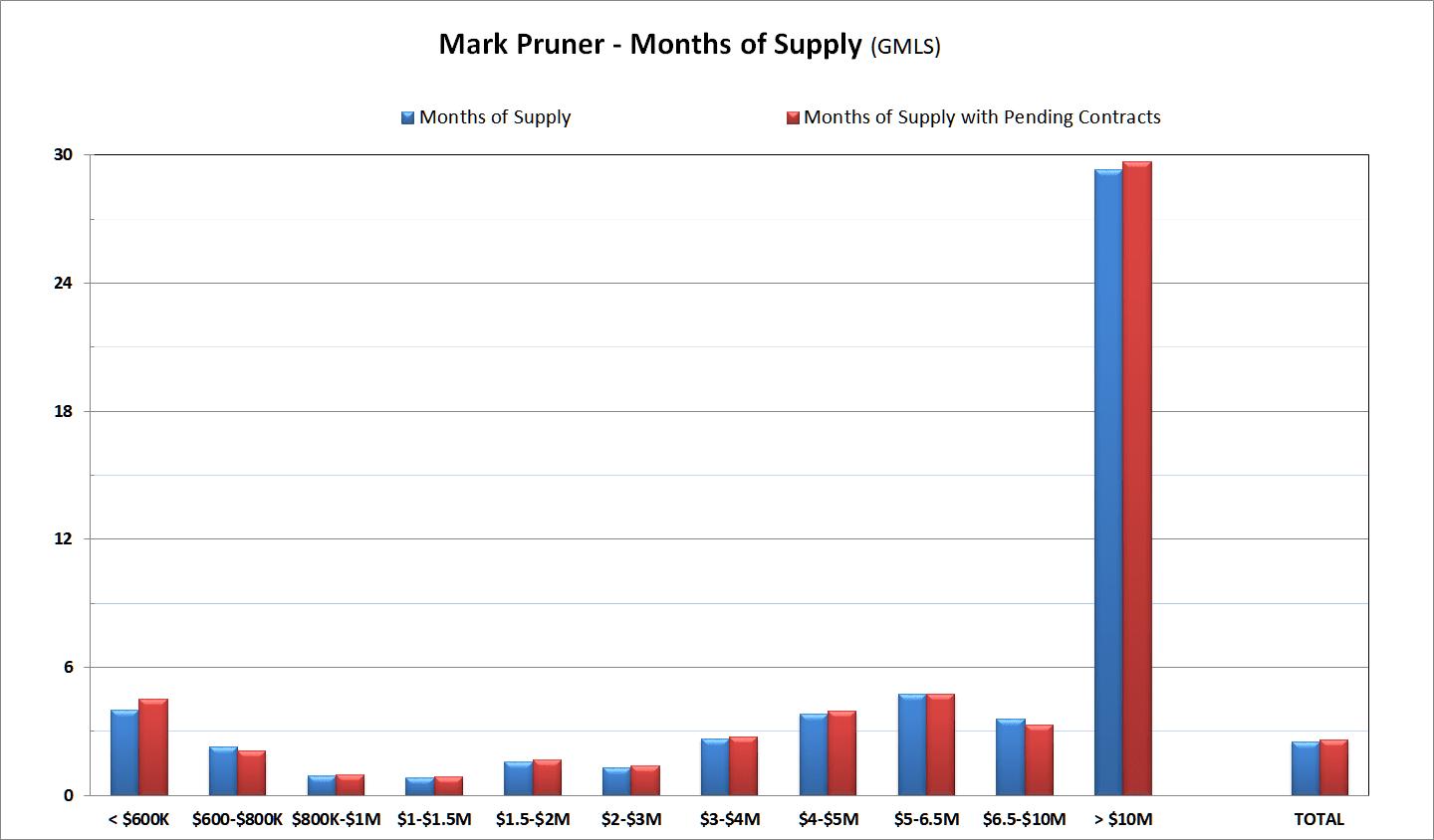

In 2021 our median price was $2.45 million up from $1.87 million at the end of 2019 or a 31% increase. This median sales price was up 6.5% from 2021’s median price of $2.30 million. Our market overall was very tight most of the year with months of supply below the 6-month dividing line between a buyers’ and a sellers’ market. The only weak part of the market throughout the year was over $10 million where we now have a 29.3 months of supply at last year's sales rate.

For a really remarkable comparison, take a look at our price per square foot. One of the reasons that our high-end had a poor 4th quarter. The sales price per s.f. minimizes the impact of a change in the mix of what is selling. In 2019, our median SP/SF was $503/SF. By 2021, it had jumped to $594/SF and at the end of last year it was $669/SF. That $669/SF is up 33% from 2019 and up 12.7% from last year.

Our ultra-high-end sales were down from 14 sales in 2021 to only 9 sales in 2022. What was even more remarkable was how much lower the sales price distribution of these over $10 million houses was in 2022. Of our 9 sales, 8 of them were under $13 million. Our highest reported sale was 435 Round Hill Road that sold for $17.6 million. Our next highest sale was for $12.8 million at 32 Grahampton Lane.

What was really dramatic in 2021 was that so many of our ultra-high-end sales last year were for big numbers; with one sale at $50 million in Belle Haven and another for $45 million in backcountry. In total sales volume over $10 million was down from $272 million in 2021 to $109 million meant a drop of $174 million in sales volume.

Now the ultra-high-end actually did better than that as we did have two off market sales at the high-end. Both sales were in backcountry with one selling for $25.0 million and the other selling for $21.9 million. Interestingly, they were both within a half-mile of each other.

Overall, the town went from total sales of $3.02 billion in 2021 to $1.94 billion in 2022 or a drop of $1.08 billion in sales. Once again though, our 637 sales for $1.94 billion in 2022 sales looks pretty good when compared to the 2019, when we had 527 sales totaling $1.25 billion. It all depends on whether you are a glass half-full or half-empty homeowner.

What is clear, is the significant drop in sales in the fourth quarter, as interest rates increased. The greatest effect of the increase in mortgage interest rates was on those sales they don’t use mortgages. This paradoxical effect is because of the knock on effects of higher interest rates.

This increase in interest rates attracted billions of dollars from the stock market to the bond market. This sent both markets down and also cratering the crypto market. CNBC calculates that the U.S. investor lost $9.5 trillion in wealth in 2022. If your $100 million in wealth went to down to $80 million you aren’t likely to buy a $10 million house. However, it looks like 85 families decided to buy a house in the $5 – 10 million price range. For those people, they are probably quite happy with their new asset allocation. Imagine taking $5.6 million out of crypto or Facebook or Tesla and putting it into Greenwich real estate.

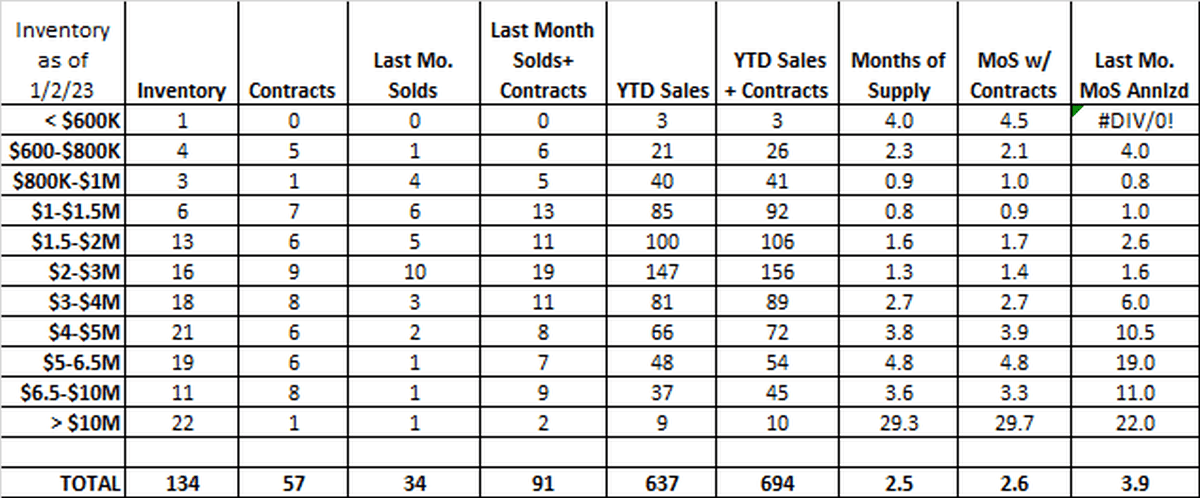

Our 85 sales from $5 -10 million with only 30 houses in inventory makes for 4.1 months of supply, still a buyer’s market if you look only at the annual sales rate. Based on December’s sales, we have 14 months of supply from $5 – 10 million. The high-end buyers look like they are being even a little more conservative, if you drop down to the next price range, our 66 sales from $4 – 5 million is only 2 less than we had in the stellar year of 2021. High-end houses are selling, just not so much at the very high-end.

The other thing that is clear is that the demand above $3 million has dropped significantly. If you take our 34 sales in December and annualize them by price range, you see a very bifurcated market. Above $3 million the annualized months of supply jumped. If you are in the higher price ranges, now is a good time to consider a price reduction.

Under $3 million, the increased interest rates hurt investors and hence our high-end market, but it didn’t it crater our sub-$3 million price range. In fact, you would think that the increase in interest rates would have had their greatest impact on our under $1.5 million market, but it didn’t. Properties under $1.5 million continue to sell like hotcakes.

At the present time we have a only 14 listings on the market under $1.5 million. At the same time, we have almost as many contracts for listings under $1.5 million with 13 contracts for listing under $1.5 million, many of which are probably selling for over list. In addition, we sold a total of 149 houses listed for under $1.5 million most of which went for over list price.

So why didn’t these sales drop. The monthly mortgage payments are definitely up a lot. The short answer is that unlike in prior years, most of our under $1.5 million buyers are not using mortgages, or expressed more precisely, they are not using mortgage contingencies in their contracts. These buyers either have the cash or were willing to waive the mortgage contingency protection in their purchase agreement in order to get a negotiating advantage over other bidders.

The first part of the year was arguably, the most competitive market we had ever seen with “months” of supply measured in weeks. Of our 637 sales last year, 224 sales or 35.2% went for over list with 56 going for 10% more than list. Another 101 went for full list price, meaning more than half of all sales in 2022 went for full list price or over list price.

And, it wasn’t just the percent over list price, some of the dollar amounts over list were stunning. Russ and I sold 113 Woodside Drive in Milbrook for $638,000 over list price after 8 days on market in April. We thought we’d done pretty well. However, it only took 3 more weeks before 432 Field Point Road went for $765K over list. The record for the year was 34 Beechcroft, which was listed for $10,175,000 and went to contract in 18 days later and closed at $11,900,000 or $1,725,000 over list. Our sale ended up coming in sixth for most over list.

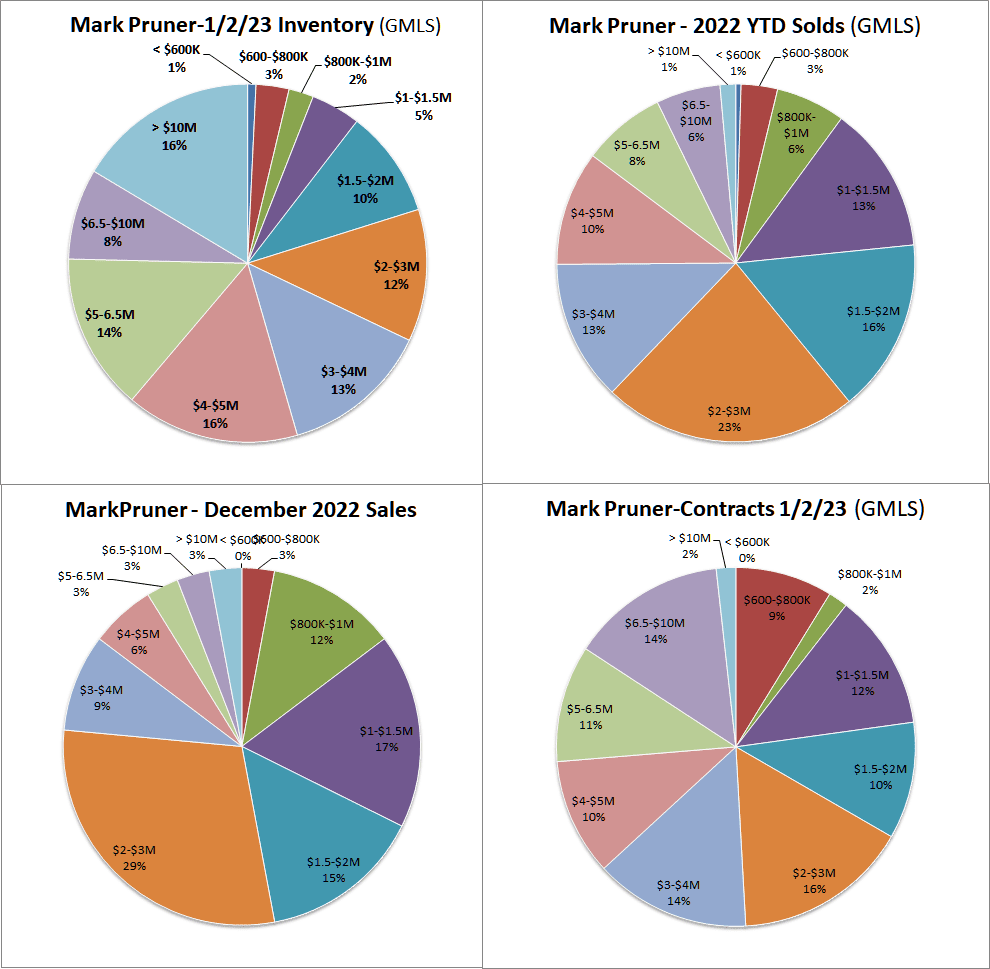

Of our 34 sales in December, 10 of them or almost 30% went for list or over list. Of those 10, all were between $950K and $4.0 million. Under $1 million we have very little to sell. Above $4 million our market is now pretty balanced and becomes more pro-buyer as you get higher in price. What is not balanced is our inventory. Our median price for the listings presently on the market is $4.4 million. Think about that, half of our inventory is over $4.4 million, while only 10% is on for less than $1.5 million. We actually have more listing over $10 million than we have under $1.8 million.

If anyone tells you they know what is going to happen in Greenwich real estate in 2023, there is a good chance that they’ve been smoking some of our newly legalized cannabis. Between, inflation, the Fed, interest rates, the Russian war, and Covid in China, the future is highly variable. I’d be shocked however if inventory get’s back to anything like normal this year. While demand is down, our inventory has been down even more.

I do expect that we will see more inventory than we saw in 2022. If we get more inventory under $3 million, we are very likely to have more sales in that price range. Also, if we get more inventory, we may get even more inventory as gridlock lessens. Right now, we have a bunch of owners that would like to sell, but they don’t have anything on the market that they want to buy. If we get more inventory, these potential sellers will have something to buy and can put their house on the market. As a result, it’s possible that inventory could rise quickly, but we still have a long way to go to get to anything like our traditional inventory levels.

As a result of our record low inventory, prices may well continue to rise, particularly under $3 million, as we are supply constrained. At the same time, many sellers, particularly, at higher prices need to look at today’s market to see if they are competitively priced.

Stay tuned ….

Stay up to date on the latest real estate trends.

Blog

Blog

Blog

What the Numbers Actually Mean for You

Blog

What Every Greenwich and Stamford Pet Owner Should Know

Blog

What Actually Matters (And What Doesn't)

Market Report

Stamford, CT

We have 8 options for you

Blog

Blog

Discover the best places to live across Greenwich

We are a dedicated group of Greenwich natives. We have a deep passion for our hometown and enjoy everything the town offers its residents from the beach front to the backcountry. That is why we don’t find you just any home, we find you the right home.

MARK PRUNER

DENA ZARRA

RUSSELL PRUNER

COMPASS

200 Greenwich Ave

3rd Fl Greenwich, CT 06830