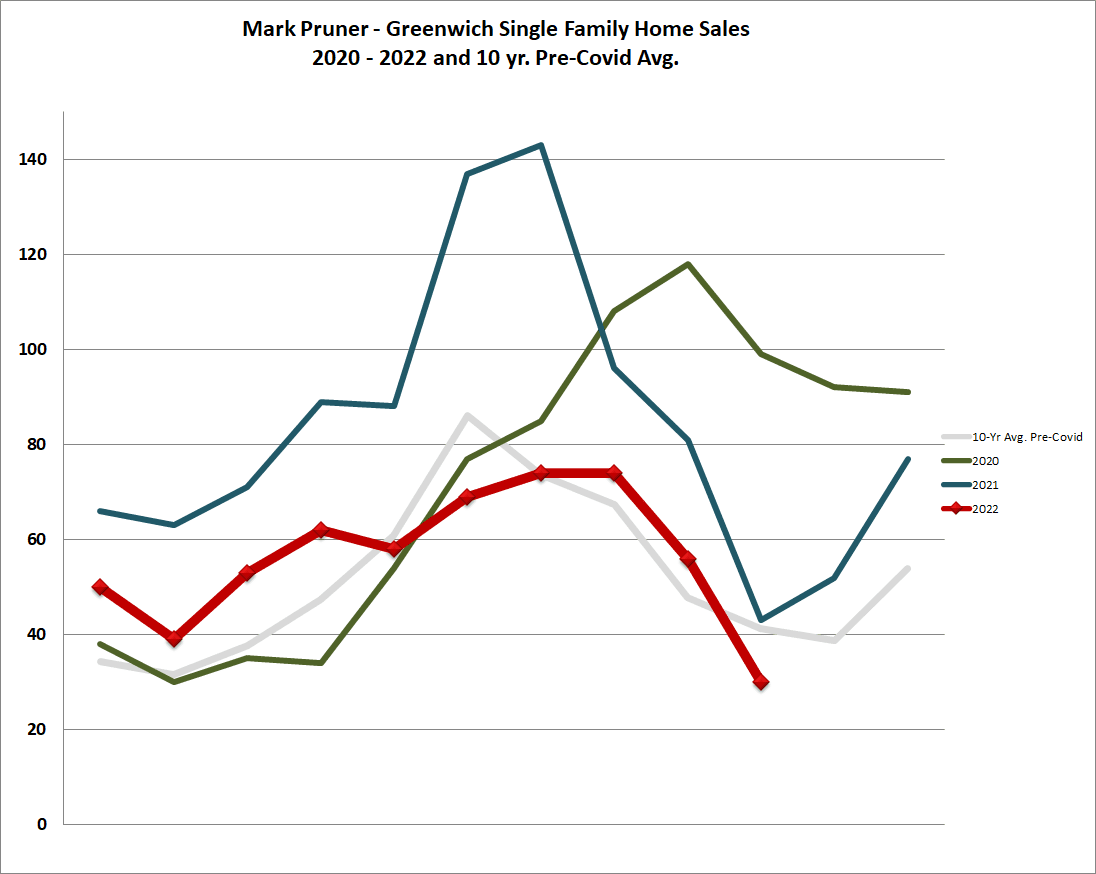

Sales Down, Inventory Down, Contracts Up

The Federal Reserve has finally strangled the Greenwich real estate market (or have they? More about that later.) However, it’s probably not in the way that the Fed expected. Last month, in October 2022, only 30 single-family homes were sold in Greenwich. This compares to 43 sales last year and 99 sales the year before that. Our 10-year pre-Covid average of 41 sales in October, so our October sales are down 27% from an “average” year.

Under $1 Million

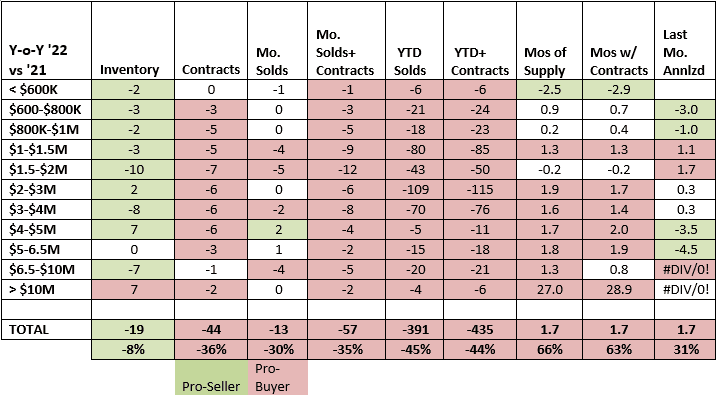

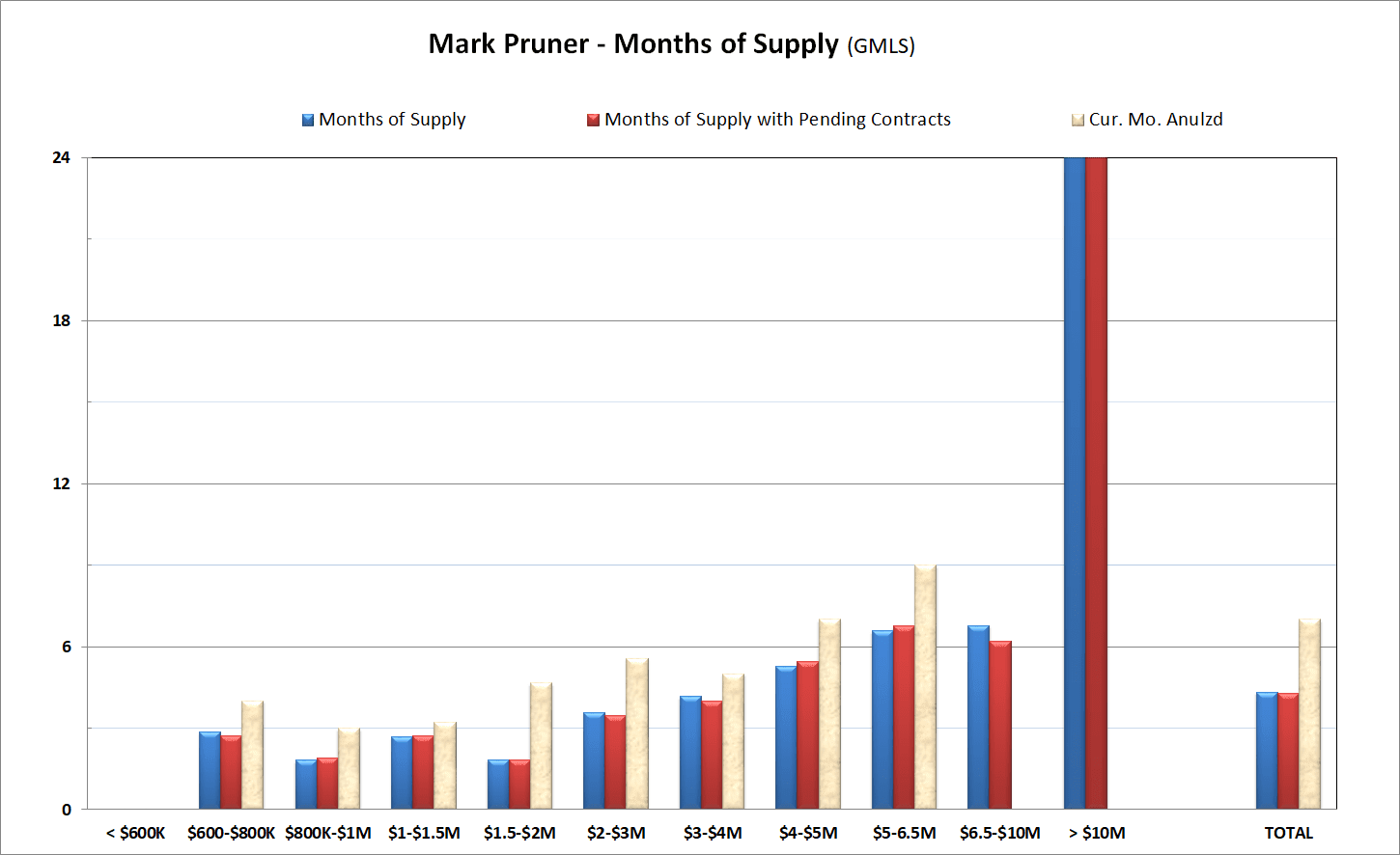

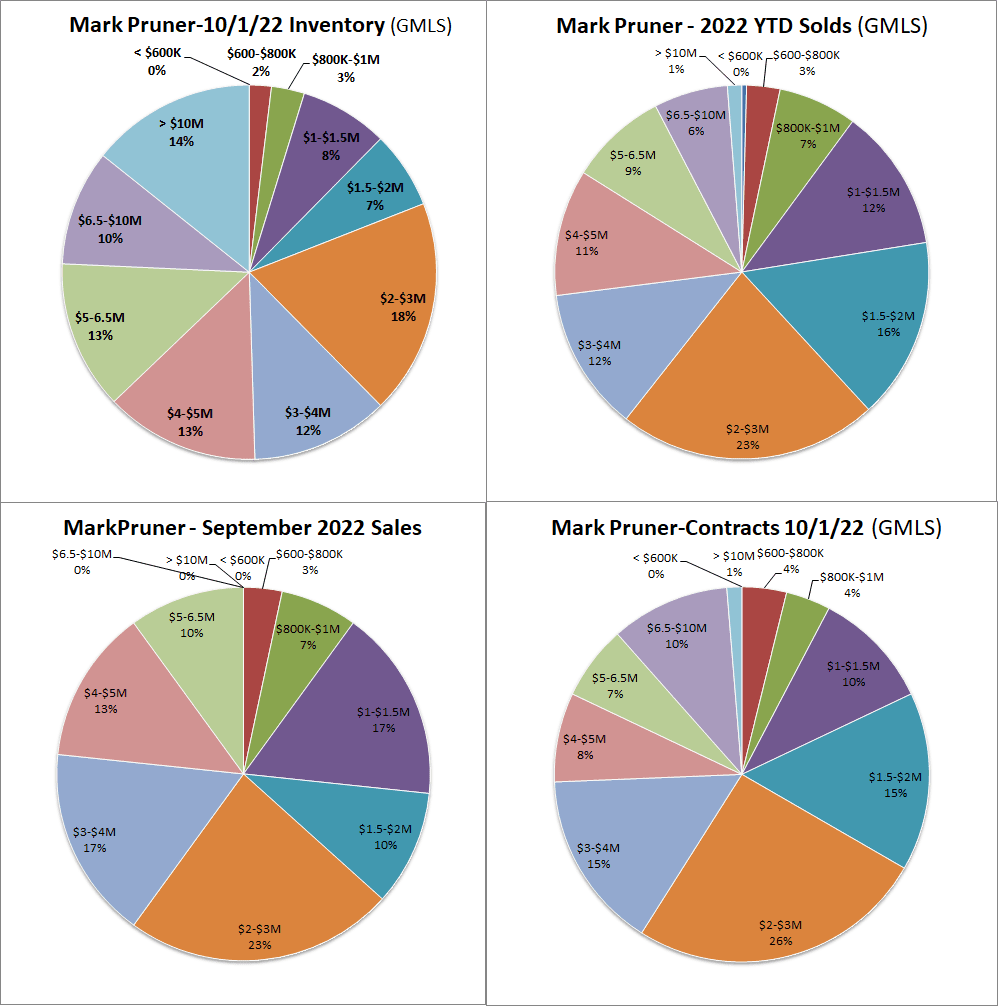

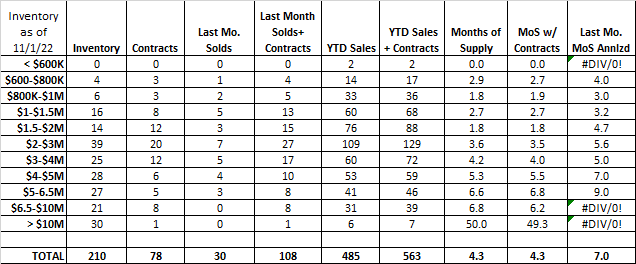

The biggest drop in October sales was in the $1 – 2 million price range, where sales were down 53% from last year. You would expect that higher interest rates would slow sales, and the lower the price range, the greater the impact. However, that’s not what we are seeing in the market. From $600,000 to $1,000,000, we had the same sales as last year, which was a total of 3 sales in both October 2021 and 2022. Our months of supply for the $600,000 - $1 million actually show a tighter market in October 2022 when you compare with October sales annualized months of supply YTD months of supply going from 5.5 months of supply for the whole year to date to 3.5 months of supply for the sales rate in October.

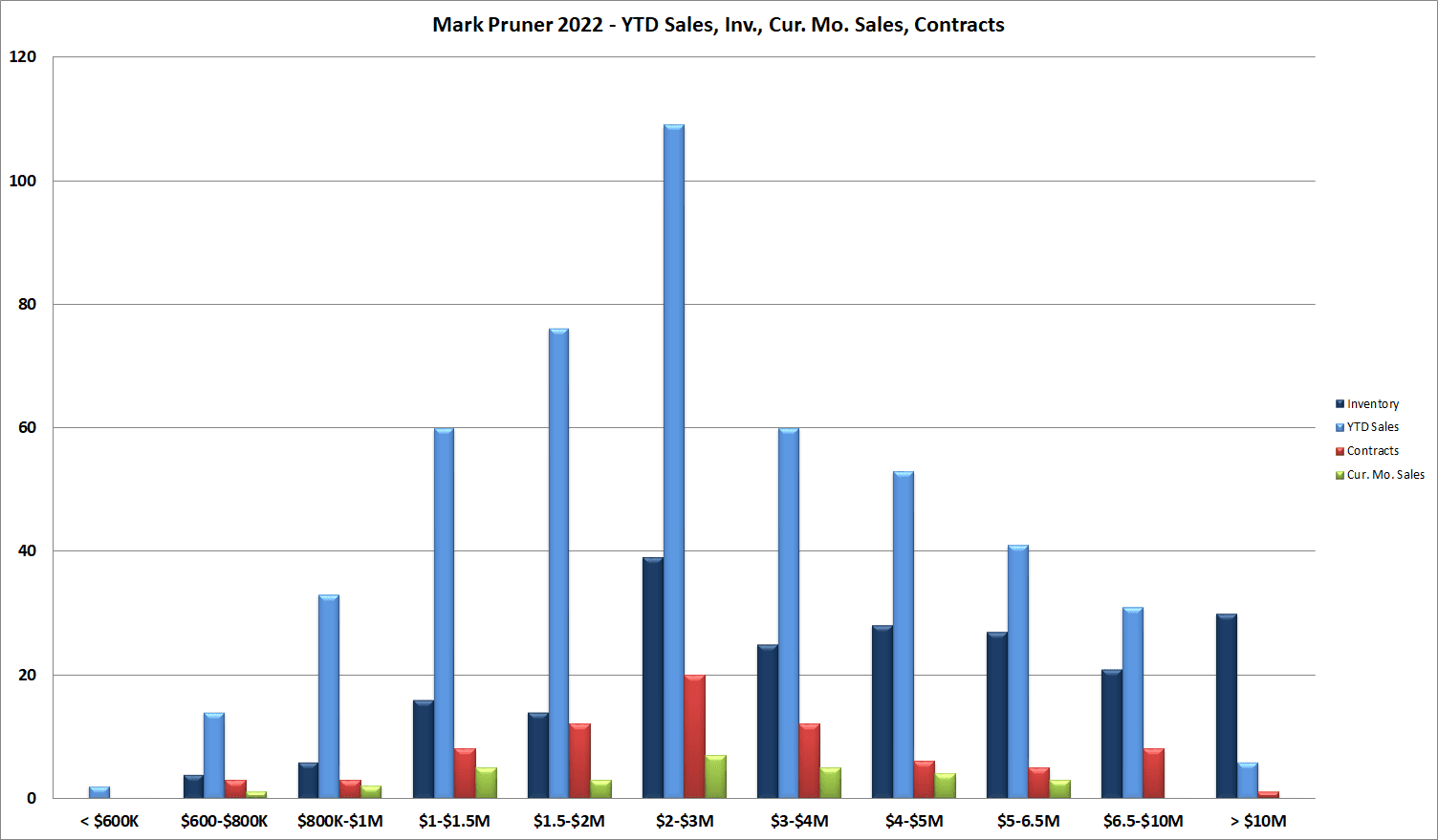

Still, you would think that having only 3 sales would be a sure sign of a weak market, but what it is really is a sign of just how little inventory we have. Under $1 million, we have 10 listings and under $600,000 we have no listings. This compares to 15 listings in that price range last year and 53 listings under $1 million in October 2019, our last pre-Covid year.

High-end Market

Where higher interest rates have most hurt the Greenwich market is over $1.5 million and particularly the over $4 million market. The correct response here is that shouldn’t be, since houses over $4 million rarely use traditional mortgage financing, so why are they hurt by higher interest rates? Not only should sales at the high end not be hurt by higher interest, but high-end sales should be increasing as higher inflation pushes people too hard assets. Hard assets traditionally see their value increase in inflationary times, and we certainly have that.

The problem is that the folks at the high end have fewer assets today. Stocks, bonds, and crypto are down by a lot. To take an extreme example, Mark Zuckerberg’s Meta stock is down $100 billion from its high last September. He’s still the 29th richest person in the world, but he’s not likely to be buying a lot of real estate properties. Then again, that’s exactly what Bill Gates did.

The higher the house price, the lower demand. We had no sales over $6.2 million last month out of 54 listings over $6.2 million. When you compare annualized October months of supply to months of supply for year-to-date sales, we see a jump of over 2 months of supply from 5.9 months of supply to 8 months of supply in the $4 – 6.5 million price range. That end of the market is getting tougher for sellers.

Not only is it uncertainty about the Fed, inflation, the economy, and interest rates; you also have an election that may well lead to even more gridlock in Washington and a war in Ukraine that could spiral into an even worse situation. Home buyers have plenty to worry about and decide the best course is to wait.

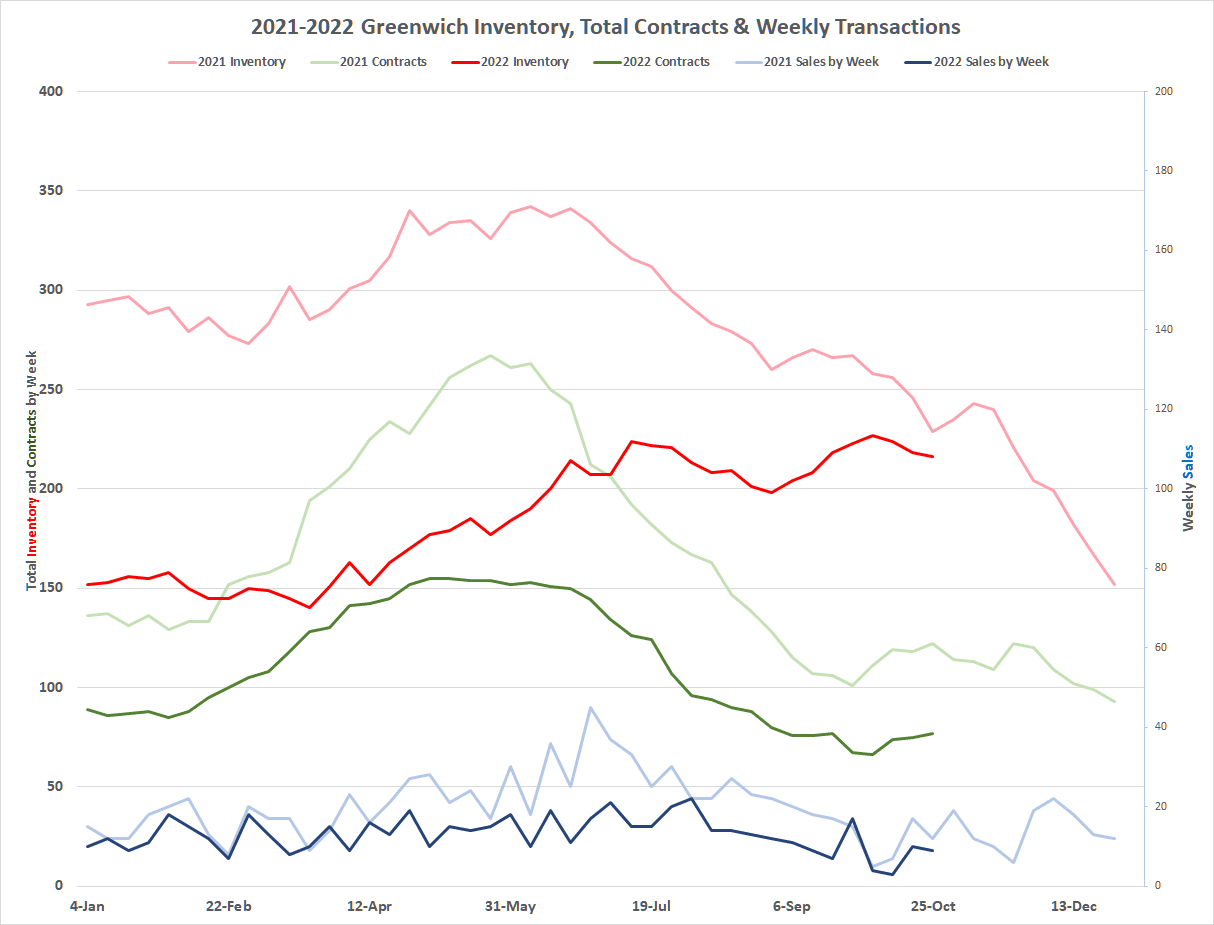

Inventory dropping again

Despite falling sales, our inventory numbers can’t seem to increase. We did see inventory go from 198 listings at the end of August to 227 listings at the end of September or a jump of 15% in just over a month. Then came October and inventory continued to shrink. This week we are back down to 207 listings.

Signs of an improving market

That’s the gloom and doom, what about those signs I mentioned at the beginning indicating that the Fed’s effort to strangle the Greenwich real estate market may not work out like they planned? Let’s start with that dropping inventory, which can only hurt sales. Well, not really. The main factor leading to dropping inventory is an increase in contracts. We went from 66 contracts at the beginning of October to 77 contracts at the end of October and this was with 30 of those contracts at the beginning of October turning into sales by the end of the month. Those 30 sales were more than replaced by an increase in signed deals.

Of the 30 sales that we had in October, an amazing 25 of those 30 sales were on the market for less than 2 months, i.e., 83% of what sold were newer listings. Eighteen of the 30 sales were of houses that had been on the market less than 30 days.

Also, most of those had been fairly recently renovated. The average build date was 1959, while the average renovation date was 2015. These 30 houses sold for an average of 102.2% of list price. Houses in good shape and priced well sell quickly. We still have a lot of motivated buyers even with the uncertainty that we have.

If you look at October sales compared to the first half of the year both the average and median sales prices are down, but this is because of the mix of what is selling. If you look at price per square feet, it is up 6.3% from the first half of the years. Our average sales price to original list price is up from 100% in the first half of the year to 102.2% in the month of October. Our days on market have gone from 44 days on market in the first half of the year to 19 days on market. This all sounds great, but the mix is also changing here, so beautifully renovated houses are selling, while older houses that need work are too often sitting.

Who’s looking to buy

Russ and I put on 35 Sterling Road a recently renovated contemporary on a private road in backcountry with a pool and tennis court for $3.29M. We got a variety of buyers; Greenwich families looking to upsize, Armonk residents looking to drastically downsize their tax bill but who wanted to stay close to friends, international buyer now that travel is back, Covid renters who have decided to stay in Greenwich and NYC buyers looking for both weekend houses and safety.

What Next?

The market has a variety of buyers and one thing we’ve seen repeatedly in the market, is that when uncertainty is removed or diminished, even when change is in a “bad” directions, people move forward. Elections are next week, and the Fed may back off the big jumps in rates. We have Olympic forces battling each other to push the market in opposite directions. (N.B. The RMS Olympic, sister ship of the Titanic, sailed on for 24 successful years as a cruise liner and WWI troop ship, despite a few bumps here and there.) Our market is sailing through turbulent times, but some of that turbulence will resolve itself.