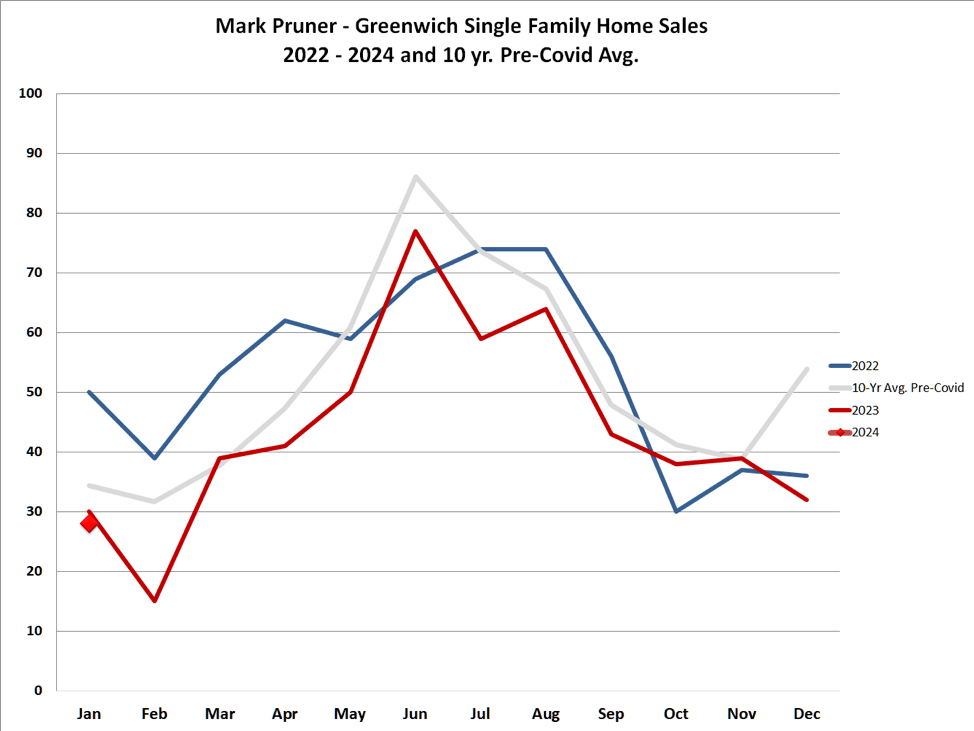

A quick glance at our monthly sales and the Greenwich real estate scene might seem pretty normal, perhaps slightly subdued, but don't let one data point fool you. January's single-family home sales totaled 28, just a tad shy of the 30 sales from the previous January. While this figure falls below our 10-year pre-Covid average of 34.4 sales, it's not too shabby and aligns fairly well with the trends we've been observing since the latter half of 2023. However, that's where normalcy takes a detour into the land of the strange.

Greenwich real estate hasn't exactly been normal since 2018, when we had 593 single-family home sales. From there, it's been a roller coaster ride. In 2019, we took a dip with only 526 sales, and then Covid arrived. Amidst the chaos, people sought refuge in more space, both indoors and outdoors. Suddenly, those vast properties in our 2-acre and 4-acre zones, which had been on a downward slide since the Great Recession, staged a remarkable comeback in 2020. The gripes about solitude on these expansive plots and the hefty upkeep costs of large houses suddenly seemed trivial, as safety became synonymous with space and on-site amenities for families confined to their homes 24/7.

In 2021, sales soared to record highs, surpassing the 1,000 mark for the year. What went less noticed, however, was the ample shadow inventory of homeowners who had been waiting to sell and were perfectly poised to supply the inventory for the skyrocketing demand. Were it not for the large amount of shadow inventory waiting to come on the market, we would never had set sales records in 2020 and then 2021. Come the latter part of 2021, that shadow inventory began to dwindle. Our inventory tightened from the lower end and gradually creeping upward in price.

By September 2021, our inventory hit record lows week after week, yet we managed to keep up with the demand thanks to a steady stream of new listings. Many of these listings were blue moons that came on and went to contract in the same month and hence were never counted in the snapshot of monthly inventory numbers done at the end of each month.

In 2022, while inventory remained low and struggled to rise, it didn't peak until September – a departure from the usual inventory peak in April or May. Consequently, 2022 sales of 639 just barely nudged above our pre-Covid average of 624 annual sales, even though the demand was there as shown by even lower days on market and more sales going over list price.

Last year, we witnessed more of the same, with Greenwich inventory hitting new all-time lows almost every month. With demand high and supply low, our months of supply plummeted to unprecedented levels, with many price ranges measured in mere weeks of supply. With inventory scarce, we ended the year with 527 sales, a number reminiscent of 2019 poor sales, but this time the low number of sales was due not to lack of buyers, but lack of houses to buy.

And then came January 2024, bringing with it a fresh batch of strangeness. January typically sees a bump in sales as some homeowners delay closing on their sale until the new calendar year, deferring their capital gains payments by another 15 months. At the same time, new inventory tends to be scarce in January, as sellers know buyers aren't keen on trudging through snowdrifts to attend open houses.

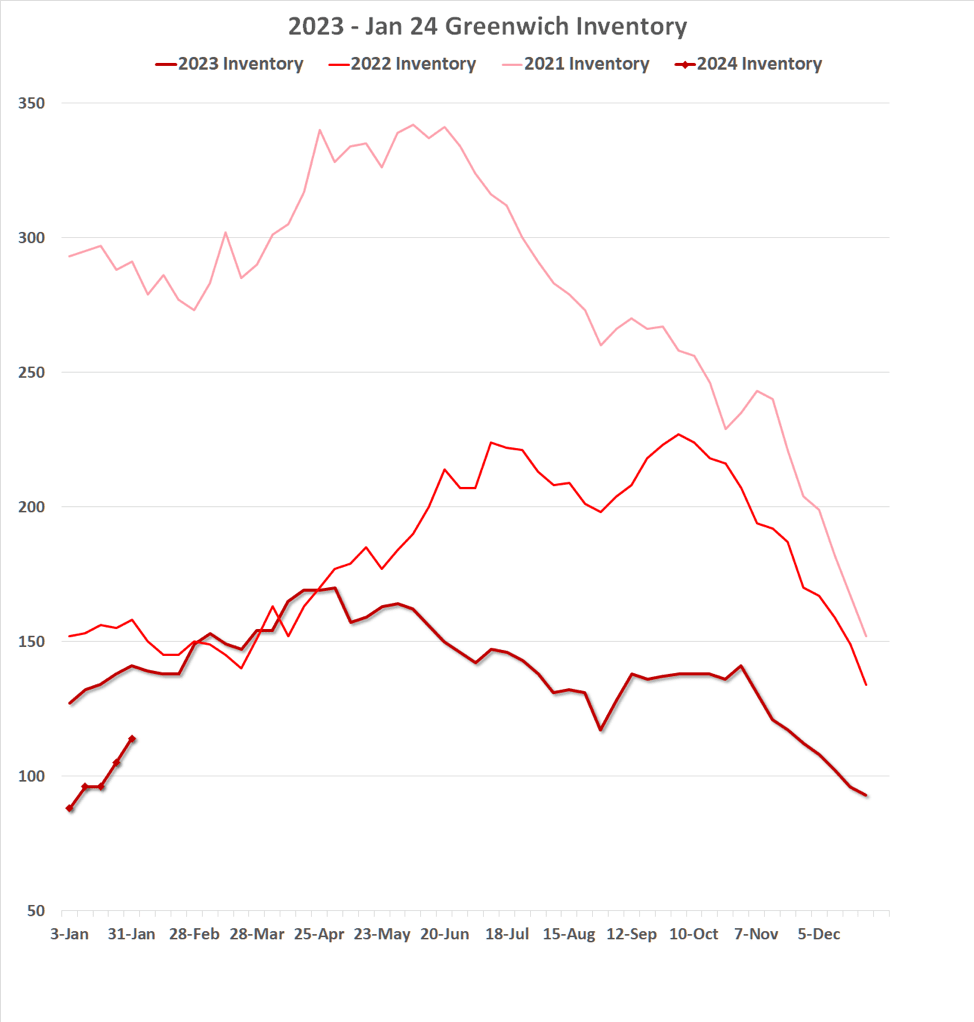

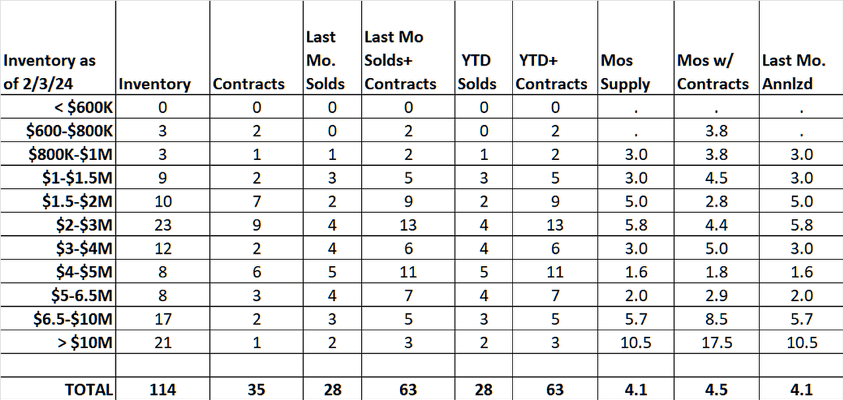

This year, while snowfall has been scant, new contracts have been even scarcer. Consequently, inventory has skyrocketed on a percentage basis. At the start of the year, we had a mere 88 single-family home listings on the Greenwich MLS. By month's end, listings had surged by 30% to 114 – a January phenomenon we've never seen before.

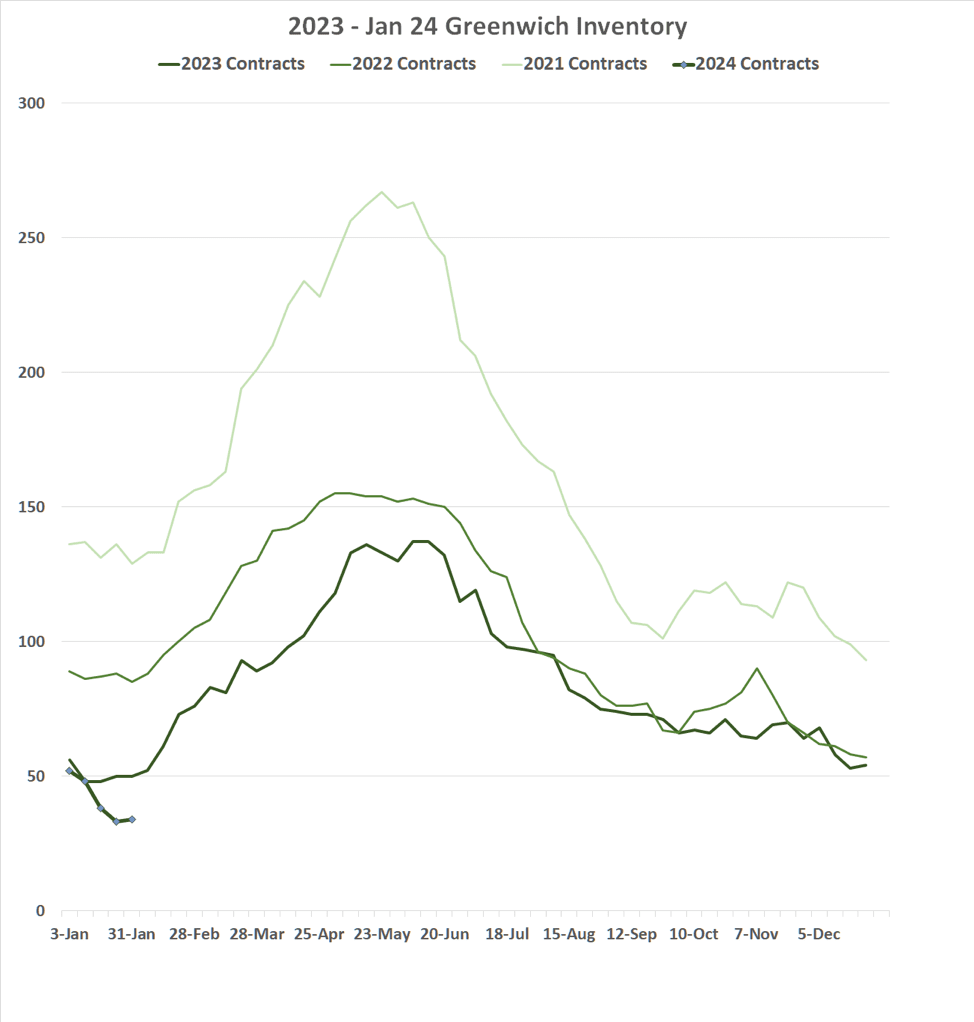

A 30% spike in single-family inventory is noteworthy in itself, but what truly stands out is the imbalance between new house listings and newly signed contracts. With 44 new listings compared to 39 last year, and a staggering 18 fewer contracts – dropping from 52 to a mere 34 contracts– it's evident why our inventory has surged.

But does this spell the end of the hot market? Not quite, 114 listings still constitute a remarkably low inventory. Anecdotally, our Greenwich Streets Team here at Compass continues to work with motivated buyers scouring the slim pickings, and reports from other agents echo similar sentiments. In fact, I've received five "In Search Of" emails in the last three days alone – a testament to the frustration buyers are facing in finding suitable properties among the sparse listings.

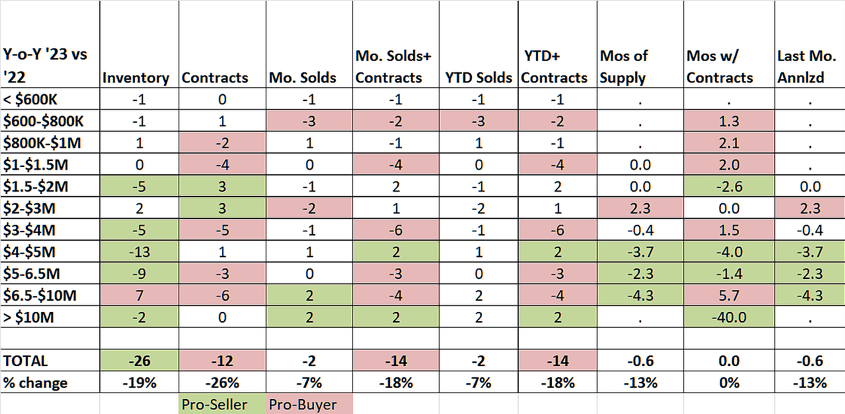

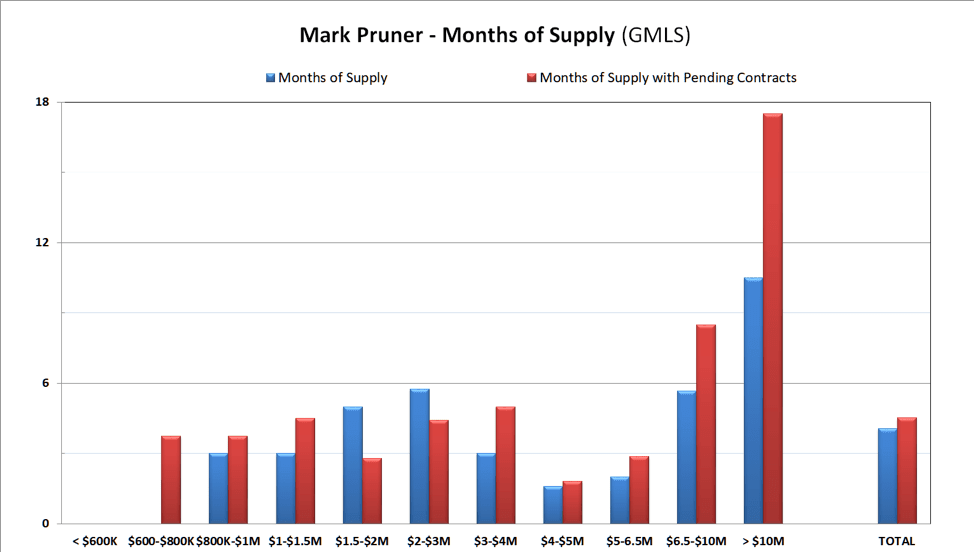

Our inventory is down 19% from last January, and the total of sales and contracts have taken an 18% hit. The most significant drops are observed in the $3 million to $6.5 million range, where we've seen 24 fewer listings. However, the $6.5 million to $10 million bracket has seen a slight uptick of 7 listings, suggesting that high-end sales may continue at near-record levels for a while longer, although much of the high-end and ultra-high-end shadow inventory has likely been depleted.

While inventory is moving in the right direction, there's still a long road ahead – both for our inventory levels and for 2024 itself. One quirky month doesn't necessarily forecast a quirky year, but it certainly makes for an interesting start.

Mark Pruner is a sales executive with Compass Connecticut and a principal in the Greenwich Streets Team. He can be reached at 203-817-2871 or [email protected].