The Greenwich April 2023 Market Report - Multiple Offers and Lower Sales

Mark Pruner | May 5, 2023

Greenwich, CT

Mark Pruner | May 5, 2023

Greenwich, CT

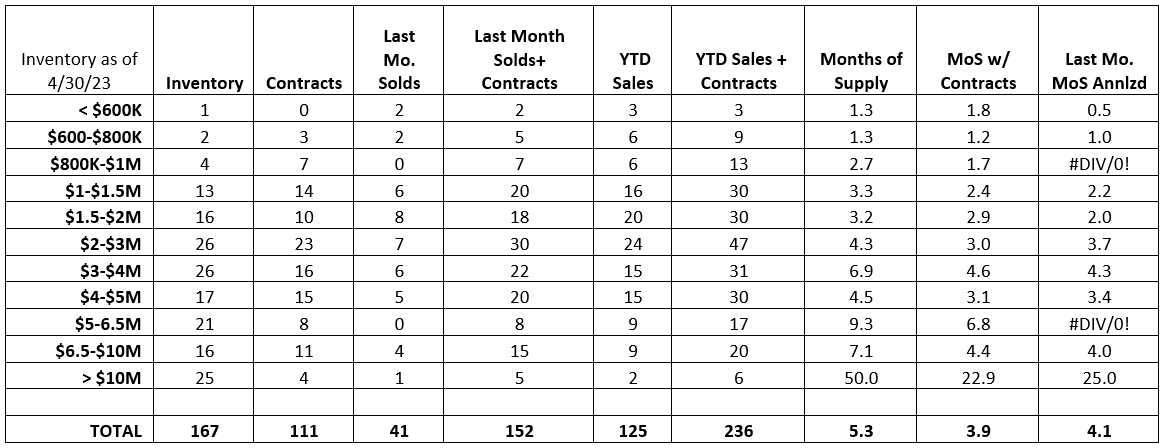

At the end of April, we had almost 3 times the number of contracts as we had sales in April. We had 111 contracts waiting to close, and 41 sales in April. These 111 contracts are just a smidge behind the 125 sales that we’ve had for the first four months of 2023.

Covid continues to drive our market. Covid pushed 3 years of sales into 18 months from July 2020 to December 2021. These record sales could only happen because a lot more people decided to list their homes for sale during that 18-month period. As a result, many of the people who would have been listing their houses this year have already sold. We had a lot fewer listings come on the market in 2022 and it's gotten worse in 2023. This year we are seeing a low mortgage rate lock-in of under $2 million.

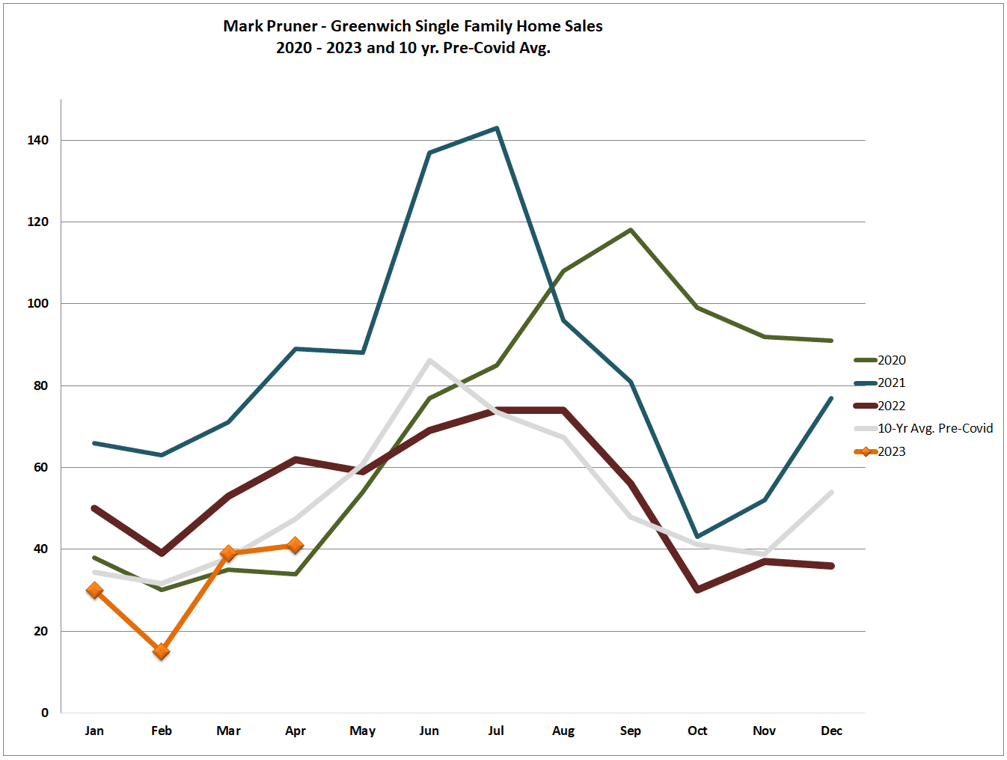

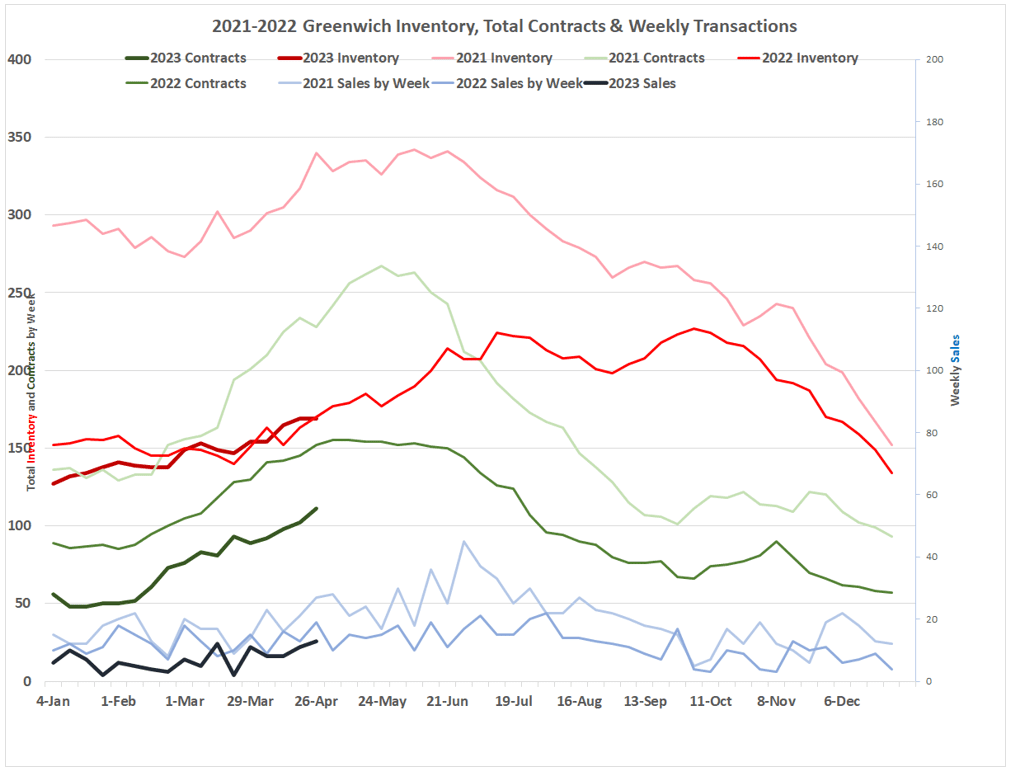

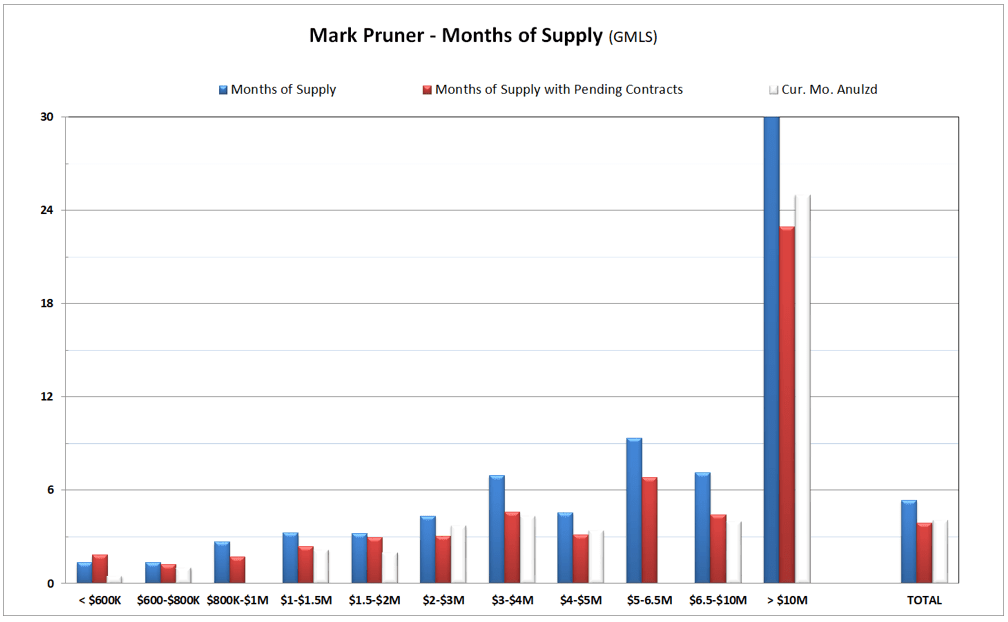

Last month’s data shows that April 2023 sales were below the 10-year pre-Covid average and only barely above March 2023 sales. These lower sales are driven by fewer listings coming on the market. Yes, our weekly inventory numbers have climbed, as they always do in the spring market, but this increase have only matched last year's record low weekly inventory. This has led to a tight market with low months of supply, particularly in the sub-$3 million price range. However, as we move up the price ladder, the market becomes more favorable to buyers.

So far this year we have had only 266 single family home listings, possibly the lowest ever. This is down 16.4% from last year very low number of new listings. In 2023 we had a only 322 listings in the first four months of the year. Curiously this drop in 2023 listings has been matched by an equal drop in demand. This drop in demand is evident, because normally a lower number of new listings would have led to lower inventory. We didn’t see a lower level of inventory even with lower number of listings, because demand fell too.

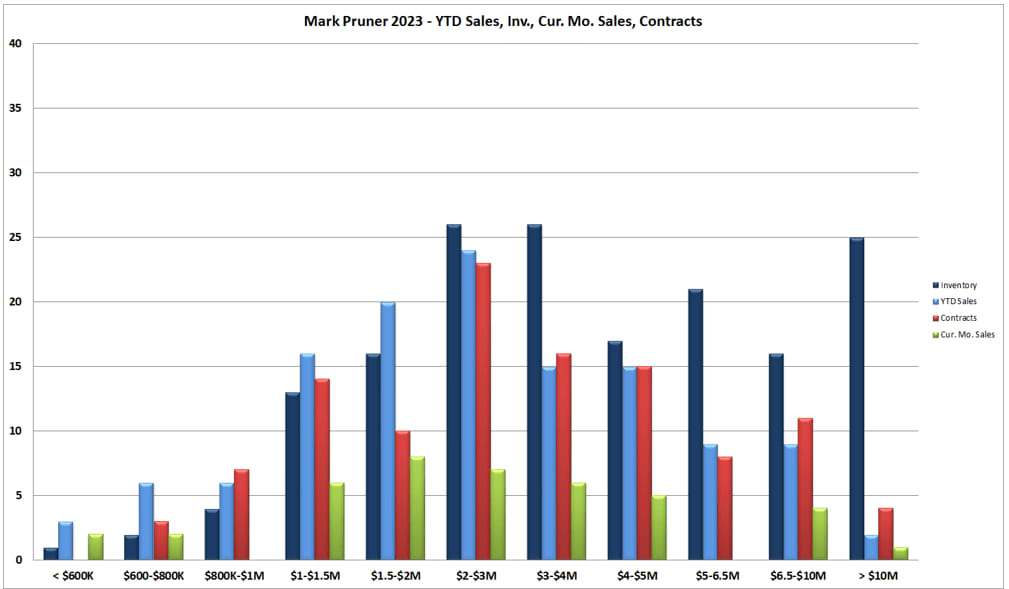

At the moment, we only have 7 listings under $1 million, which is limiting options for first-time buyers and those looking for more affordable properties. The shortage of inventory is particularly acute in the single-family home (SFH) market under $600,000. There is only one listing available, with no contracts signed in April. This means that buyers in this price range are facing intense competition, with few options available to them.

At the other end of the market, above the $5 million mark, the market is shifting towards a buyer's market. There is plenty of inventory available over $10 million with 25 listings and only 2 sales over $10 million including Russ and my April sale for $10.4 million in mid-country. So far, the highest sales price this year, and the only other sale over $10 million, was in Deer Park for $13.5 million. With 25 listings and 2 sales over $10 million you are looking at 50 months of supply or over 4 years of supply, making this a buyer’s market, (Or does it? See more about this below.)

On the better news side, if you throw in the 4 ultra-high-end contracts and assume they take an average of 1.5 months to close, our months of supply over $10 million is more than cut in half to only 23 months of supply. Of those 4 ultra-high-end contracts, three out of four are listed at the lower end of the price range, between $10 and 12.5 million. The median days on the market for those four contracts is 550 DOM.

Where sales are really tough is for those houses listed over $18 million, where we have no sales and only one contract. The median DOM for listings over $18 million is 305 days on the market. (It’s actually higher than that as many listings had their days on the market reset by being off the market for 90 days or more over the winter.)

You can however argue that in some ways, we have an inventory shortage of new over $10 million listings. Over $10 million, we have only had 8 new listings in March and April. However, 3 of those 8 listings were renewals of listings that had expired. Those 3 ultra-high-end listings coming back on have had 452, 329, and 176 days on the market. In the last two months, we only had 5 new listings over $10 million.

When something good does come on the market, even over $10 million, and is priced right, there are people ready to move fast. Our mid-country listing went to contract in 10 days and another listing at $10.5 million went pending (i.e., a non-contingent/binding contract) in an amazing 4 days.

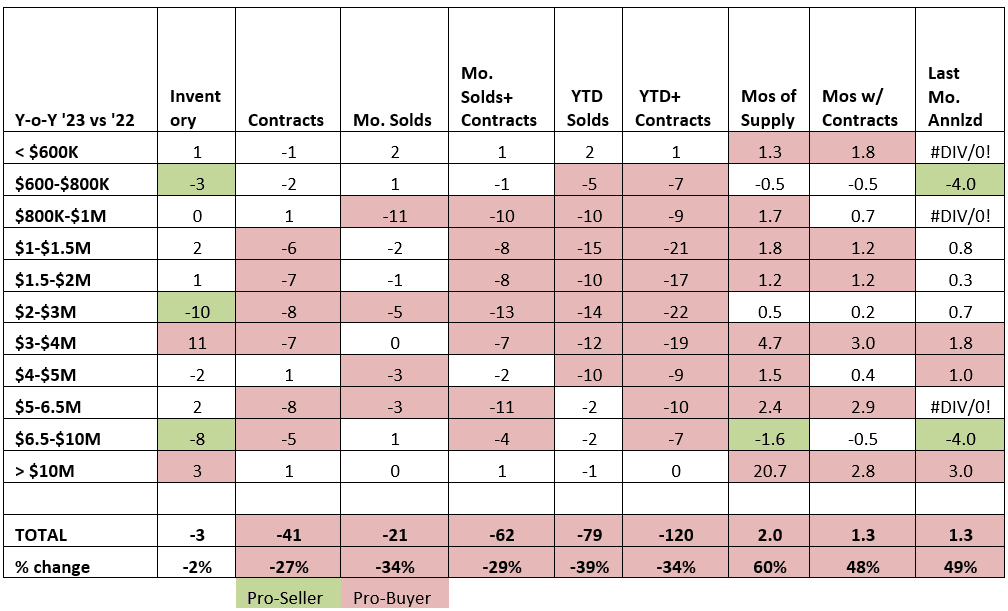

If you drop down to the next price range $6.5 – 10 million, we have only 16 listings with 9 sales to date and another 11 contracts meaning you are looking at 4.4. months of supply. It looks like those buyers that can afford these high-end houses have dropped down a few million dollars and are buying up the inventory we have. For 2023, we are down from 24 listings at the end of April last year to only 16 listings this year. If you have a house between $6.5 million and $10 million, now might be a good time to list.

It is however a narrow band, dropping down to $5 – 6.5 million and listings are up slightly to 21 listings. (BTW: I use $6.5 million rather than $7.5 million to break up the $5 - 10 million range as that more evenly divides up the listings, e.g., 21 listings from $5 - $6.5 million, with only 16 listings from $6.5 to 10 million.)

In this price range, we have had 9 sales and 8 contracts. Not bad, but not the 12 sales and 16 contracts that we had last year at this point. We are looking at 9.3 months of supply, but throw in the 8 contracts and we drop to 6.8 months of supply. Even though this is up from last year, it actually looks pretty good, compared to the pre-Covid market in this price range. In April 2019, we had 9.8 years of supply from $5 – 6.5 million with 59 listings and 2 sales. It’s just that last year in this price range, we had a tight 4.5 months of supply. It all depends on what you want to pick for your base year.

Overall, our sales YTD are down 39% compared to last year and contracts are down 27%. Having said that, sales in all but our highest price ranges are severely restricted by inventory shortages. Given our 111 contracts waiting to close, May 2023 should be a better month for sales. Then again, our 10-year pre-Covid average for May sales is 61 sales. Stay tuned, 2023 has been a see-saw year, and we should beat the average, but then again, who knows……

Stay up to date on the latest real estate trends.

Blog

What the Numbers Actually Mean for You

Blog

What Every Greenwich and Stamford Pet Owner Should Know

Blog

What Actually Matters (And What Doesn't)

Market Report

Stamford, CT

We have 8 options for you

Blog

Blog

Market Report

Greenwich, CT

Discover the best places to live across Greenwich

We are a dedicated group of Greenwich natives. We have a deep passion for our hometown and enjoy everything the town offers its residents from the beach front to the backcountry. That is why we don’t find you just any home, we find you the right home.

MARK PRUNER

DENA ZARRA

RUSSELL PRUNER

COMPASS

200 Greenwich Ave

3rd Fl Greenwich, CT 06830